Strategic Global Intelligence Brief for October 7, 2019

By Chris Kuehl, Ph.D., NACM Economist—

Short Items of Interest—U.S. Economy—

Economy Is in a Good Place—

In advance of the release of the Fed minutes, there have been some encouraging words out of the Fed. Perhaps the most interesting comments have come from Esther George of the Kansas City Fed. She is a hawk who has dissented from the Fed decision to lower interest rates the last two times it has met. She would have been more comfortable with rates at 2.5% than the current 2% and has suggested in the past that rates near 3% would make more sense. It is significant that she is now offering the opinion that rates would trend lower should the stress in the global economy slow down growth in the U.S. enough. This is far from a statement supporting a rate cut in the near future, but it signals she remains a pragmatist and will not resist a rate reduction if the economy stutters. At the same time, she has warned that a rate cut will not suffice if the economy is in real distress.

Fixing Liquidity in the Market

For two days, the Fed was very aggressive as far as the overnight lending market was concerned. A liquidity crisis had developed as banks and business suddenly started to worry about their liquidity and cash positions. There was a run on these overnight loans and interest rates were jumping up in response. The Fed injected a great deal of money and calmed the markets, but now it has to grapple with how to keep this from repeating. Further, it will have to assure the financial community this was not done as a means by which to stimulate the economy. If that were the case, it would be assumed the Fed is worried about the need for stimulus, which would lead to expectations regarding interest rate policy.

Trade Deficit Widens

Given all the angst over trade wars and tariffs, one would have expected U.S. consumers to have reduced their buying of imports by this time. Consumers are actually buying more imports than in the past, but the source of these imports has diversified. The trade with China has been altered, but not as much as had been expected as the appetite for these goods has barely been dented. The U.S. has also exported more—especially oil and vehicles as well as food. We still buy far more than other nations and that will keep this imbalance intact.

Short Items of Interest—Global Economy

NBA's Interesting Stance

Anyone who was laboring under the impression the NBA operates under any principle other than maximizing profits will have been disabused of that notion with the stance it has taken on Hong Kong. The GM of the Houston Rockets voiced support for the protestors in Hong Kong, which irritated the Chinese. That prompted the NBA to condemn the Rocket's General Manager. Seems that offending a growing market was more important than supporting people demonstrating to retain their freedom from an autocratic regime.

More Center-Left Gains in Portugal

It was only a year or so ago that political pundits were predicting the demise of the center left in Europe. The populists from both the right and left were on the rise and the centrist parties seemed to be fading fast. Now, the situation is radically different with the center left scoring victory after victory in nations as diverse as Spain, Denmark, Sweden and Finland. The latest victory was in Portugal where the center-left Socialists got 20 more seats than they had before with 37% of the vote. They still need to cobble together a coalition, but they have a stronger position from which to operate.

U.S. Turns Its Back on Kurdish Allies

During the long war in Iraq, the U.S. had only one reliable ally. That was the Kurdish Peshmerga operating in the north of the country. The government of Iraq was often at odds with the U.S. and its troops were less than effective, but the Kurds were steadfast. They have been rewarded for that loyalty by Trump's decision to stand by and allow Turkish troops to attack the Kurds in Syria. The U.S. has essentially sided with the increasingly autocratic President Erdogan of Turkey against the allies that fought with the U.S. against Saddam Hussein, al-Qaeda and ISIS. To note that the Kurds have been shocked is an understatement.

China May Not Be in the Mood to Deal

There has been a consistent narrative regarding the trade war between the U.S. and China. It has revolved around the ambitions of Trump as regards his reelection. It is assumed the U.S. is in command of this situation. The thought is that as soon as Trump decides to back away from his position a bit, the Chinese will jump at the opportunity and he will be able to deliver a victory just in time to boost the U.S. economy. China, however, has not seemed all that eager to make a deal and it is not clear it would accept anything other than near capitulation from the U.S.

Analysis: In the last few weeks, the Chinese have been taking various issues off the table and are sounding very firm on their unwillingness to bend on state subsidies or the construct of their industrial policy. The only concessions they seem ready to make involve buying more product from the U.S. and perhaps becoming more aggressive on protecting intellectual property. The impact of the tariff war on China has been significant, but it is not by any degree a crippling blow. The bigger issue for China's leaders is how they are perceived in the world and domestically. A deal with the U.S. that doesn't favor China in some way is not going to be acceptable. Given Trump's tendency to brag about his every move, the Chinese do not want to appear to have been the weaker player. Trump may think he can pull off a deal at a time of his choosing, but unless the deal favors China in some manner, it will likely not give in. That might still benefit Trump politically, but it will not have a positive impact on the economy as a failed deal will certainly spook investors and the overall global business community.

Global Recession Nearing?

The good news is the U.S. economy still appears to be pretty healthy despite the challenges that have started to appear. The consumer remains in a good mood, the rate of unemployment is down to a 50-year low, inflation is not showing its ugly head and there have even been some sectors that have surged a little (most notably health care and energy). That is the good news. The bad news is the U.S. is nearly alone in sporting any of this good news. The rest of the world appears to be teetering on the edge of recession and some of these countries are already there. The real question for the U.S. and the world is what happens now. Does the global slide towards recession eventually take the U.S. down as well or does the U.S. manage to bring the rest of the world along with it?

Analysis: In 2017, the rate of global growth was 3.7%. That was seen as pretty anemic compared to what had been the case in prior years when growth numbers were routinely in the 5% range. The current rate of growth is even worse—down to 2.9% and likely dropping even further in 2020. The challenge started with the decline in manufacturing as the trade wars affected export and import numbers. The decline has been spreading to other sectors since—everything from the financial community to retail to energy and construction. The slowdown drags everybody down with manufacturing, as that sector has been as key factor in every nation's export and import community. The U.S. and China have been locked in the most serious of trade battles, but this is not the only one.

The trade war between Japan and South Korea has damaged both of their economies and there have been tensions between India and China that have compromised trade. Europe and the U.S. have been at odds with both sides hitting the other with tariffs and other restrictions, but the biggest issue for the EU is the ongoing battle with the U.K. over the terms of Brexit. This conflict has been responsible for the decline in both the U.K. and Germany.

Then, there are the internal issues and failures throughout the world. Brazil is fast becoming a global trade pariah under Jair Bolsonaro and Argentina seems poised to head back to the bad old days of Peronism with the resurgence of the Kirchner faction. Many of the nations in the EU remain in bad shape financially (Spain, Italy, Portugal, Greece). In short, there is a lot of blame to spread around in global slowing. Recovery from the downturn will depend on the U.S. If the U.S. decides to reverse course and emerge again as the world's advocate for free trade, the rest of the global business community would likely respond and growth would improve. Such a move is not going to take place under Trump, however.

Pension Reform Controversy in France

The pension system in France is one of the most convoluted in the world as there are dozens and dozens of differing systems in place and many are through the government. This is the result of decades of union negotiations that created very specific plans for a wide variety of professions and groups. The problem is this system locks people into jobs and careers and it is very hard to switch careers and keep the pension intact. President Macron's plan has been to consolidate these systems into one common plan based on points and thus allow more people to switch employers or careers as well as have a means by which to more easily come in and out of the workforce. The problem is that each of these pensions are intensely popular with the people that are receiving them and they fear the reforms will reduce what they are currently receiving. In many cases, the new system will provide more for people, but there is considerable distrust even among those who stand to benefit.

Analysis: The French experience is a very common one—nothing upsets people more than messing with their retirement and pension systems. The fact is people who are relying on these systems are especially vulnerable as they have no options should something go wrong. It is not as if they can get back in the workforce. The vast majority have no other means by which to earn money. They have to rely on these plans for the rest of their lives and with people living longer, that is a bigger and bigger challenge.

At the same time, the costs of these schemes have dominated national budgets all over the world. The biggest share of the U.S. budget goes to Social Security and Medicare. For almost every other nation in the world, the situation is the same. The costs were not expected to be this large when the systems were established, but people have been living far longer than expected. The U.S. system basically assumed the lifespan to be around 66 to 70. Today, the average American lives well into their 80s and even 90s. This is the same pattern all over the world.

Data to Watch for This Week

There will be data on inflation, consumer sentiment and the disposition of the Fed this week. Not that this will be the definitive data that defines the future of the economy, but it will certainly shed some light on where things stand right now. It will either make the chances of recession seem more likely or will reassure to some degree that a major downturn is not really imminent.

Analysis: On Wednesday, there will be a release of the Fed minutes from their last meeting. These will be more gripping than usual as this was the meeting where three of the members of the Open Market Committee dissented from the position ultimately taken. Both Eric Rosengren from Boston and Esther George from Kansas City opposed the idea of lowering rates by another quarter point while Jim Bullard from the St. Louis Fed wanted to lower them even further. It is a rare sight to see both hawks and doves deviating from the opinions of the others. The minutes will likely reveal the thinking of the other members such as Richard Clarida, Lael Brainard and John Williams. Randy Quarles and Michelle Bowman will also weigh in, but they have more direct responsibility for regulation and the small bank sector respectively.

There will also be data released regarding inflation. The Consumer Price Index will likely show a gain of around 0.1% over last month and a gain of around 1.8% year-over-year. This is hardly high inflation, but it is high enough to suggest a fairly robust pace of overall growth. These numbers are creeping closer to the levels the Fed has been seeking. Most of the inflation data has been pointing upwards of late, but not by that much. The Fed pays close attention to the personal consumption expenditure numbers and these have been trending up as well.

There will be data related to consumer mood from the University of Michigan on Friday. The expectation is that it will trend a little lower than has been the case of late. The most important factor for the consumer is still the job market. This has remained healthy enough, but there have been other factors that have been worrying the consumer—everything from the impact of the trade wars to the impending election chaos.

Mixed Bag as Far as Job Numbers are Concerned

The total number of new jobs added was a bit lower than has been the case over the last year or so, but the gain was still respectable. The interesting number was the overall rate of unemployment as it has now fallen to 3.5%, the lowest point in 50 years. This would be an unadulterated piece of good news were it not for the fact this decline in joblessness has not come with the expected hike in wages. The Phillips Curve has always kicked in by this point—a rise in wage inflation that coincides with the shortage of workers. This has not been the case this time and that has altered the usual patterns.

Analysis: Because there has not been a higher rate of inflation due to higher wages, there has been hesitance to hike the Federal Funds Rate. There are also signs consumers are spending a little less than would be expected. They are not getting paid as much since qualified labor is in short supply. People without the necessary qualifications are being hired and they do not command the high wages that would be expected with unemployment rates this low. There are now very few people on the sidelines as far as jobs are concerned. Those that remain unemployed are either in the wrong place at the wrong time or they are holding out for a specific job at a specific rate of pay.

A Plea for Honesty

I am not naïve. I know full well that few really want to be honest. One can drive oneself crazy trying to find honesty. After all, the Greek philosopher Diogenes spent a lifetime in search of an honest man and thus founded the cynic school of thought. We are routinely lied to; it can drive one to distraction. I especially like the assertions that something was done for my convenience when it is anything but. I check into hotels that no longer provide decent room service meals to make life easier. What? How is being handed a bag of fast food making MY life easier? How is forcing me through hours of an automated message system for my benefit as is asserted? The list goes on and on. That is why I dearly love the ones who are honest with me.

I ran across a little coffee shop with a sign in the window. "I don't keep regular hours. I have three kids, three dogs, two cats, an incontinent hamster, a beloved gramma with dementia and a sometimes-unhelpful husband. I don't get enough sleep on a good day. Some days I just can't get here on time and other days I just don't feel like it. I will open when I can. When I do, there will be excellent scones and cupcakes and whatever else I feel like making. The coffee is great and I am generally friendly. I would say I am sorry for the inconvenience, but I really am not." THIS is a coffee shop I would go to EVERY day—assuming it was open!

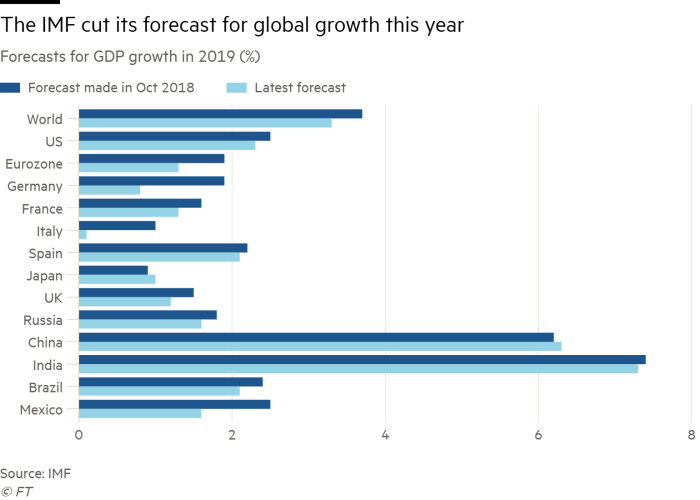

The IMF Forecast for Global Growth

The International Monetary Fund (IMF) has been sounding the alarm on global growth for some time. This year marks the first time that most of the nations have been expected to see shrinking growth. The past patterns have always shown at least one major region of the world still in growth mode, but at the moment, it appears everybody is in decline to one degree or another. This is similar to the situation that existed at the start of the recession in 2008.