Strategic Global Intelligence Brief for March 12, 2019

Short Items of Interest—U.S. Economy

Retail Data Has Been Rocky

The expectation was that retail sales would be flat at the start of the year. This was based on the fact that sales were off at the end of last year. The initial report from December of 2018 has shown a decline of 1.2%, but the revisions to that data showed a further decline of 1.6%. This had been unexpected given how robust holiday spending had been up that point. This led most to conclude that improvement at the start of the year would be minimal. More than a few had projected even further decline. Instead, there was a very modest gain of 0.2%. This is nothing to set hearts on fire, but it is certainly better than further retreat. The question now is where numbers go from here. Consumer confidence has fallen a little but is still high. However, there are more concerns starting to manifest—everything from inflation to job security and the impact of trade fights.

Is 2% Inflation Target Still Appropriate?

It has been an article of faith for some time—the level of inflation the Federal Reserve should tolerate is no more than 2%. The majority of the world's central banks are in agreement. Most tailor their interest rate policies to keep the rate at or slightly under that level. This assumption has been questioned for some time—mostly by those who think the central banks can leave more stimulus in place. Fed Chair Jerome Powell has now come out on the side of considering change, but he hastened to point out that there needs to be far more research and that any change would be highly incremental. The fear is that inflation can build up momentum and then become hard to control later—forcing very high interest rates and other aggressive moves.

China Deal Breaking Down?

It is often the case that trade deals get very sticky right at the end as all the toughest provisions are usually left to sort out until the last minute. Sometimes these provisions scuttle the whole deal. Other times, it is drama for the sake of drama. It is hard to tell what the situation is with the U.S. and China, but suddenly there is some doubt over the timing of any deal. The sticking point is enforcement. The U.S. wants to be able to impose penalties unilaterally in the event they think China is not complying. China wants a system that is mutually agreed on so they are not subject to arbitrary and capricious decisions made by Trump or whoever becomes the next president.

Short Items of Interest—Global Economy

Grounding the Boeing 737 MAX 8

It is far too early to know the similarities and differences between the crash of the Lion Air jet in Indonesia and the crash of the Ethiopian Airlines plane. There are a few issues that look similar, but there are also key differences. The planes have been grounded by several nations pending investigation—China, Indonesia, Singapore and Australia. The U.S. and the EU have indicated no such move is planned. The Lion Air crash was attributed to a combination of pilot inexperience and a system that can place a plane in jeopardy under certain circumstances, but it is not known if that was the same issue with the Ethiopian plane.

Where the World Agrees with Trump

The relationship between Trump and the traditional allies in Europe has become frayed and nearly broken. But in the states of Eastern Europe, Trump is held in far higher esteem. These are the fellow populists in places like Hungary, Poland and the Czech Republic. The three issues that stand out include his position on immigration, defense and China. These nations have been threatened by mass migration and competition with China. Also, they really don't trust the Europeans when it comes to their defense.

Global Oil

Now that OPEC and Russia are essentially singing the same tune, it appears that oil prices will be climbing towards the $80 and even the $90 level. They will likely stay there through the summer months.

Reaching Consensus on Europe's Future Will Be Tough

Last week, French President Emanuel Macron put forth an impassioned plan to unite Europe—a very deliberate attack on the movements that have been collectively labeled populism. His vision was of an expanded European Union that would move the region even closer to common goals related to everything from the environment to immigration to economic development. It was a direct challenge to the populism that has led to the Brexit move by the U.K. and the rise of parties like the National Front in France, the Five Start Movement in Italy and the Alternative fur Deutschland (AfD)in Germany. It was an ambitious manifesto to say the least, but it will go nowhere unless there is support from Germany. Given the comments by the new leader of the Christian Democratic Union (CDU), that support will not be forthcoming anytime soon.

Analysis: Annegret Kramp-Karrenbauer was Chancellor Angela Merkel's chosen successor to head the CDU. If the center right is able to hold on to power in the Bundestag, she will become Chancellor. In winning control of the CDU, she had to fight off a serious challenge from Friedrich Merz, a much more conservative leader who still commands a loyal following in the CDU. His supporters will keep the CDU focused on some of their key issues—immigration and assertions of national sovereignty. There is not much support in this group for the kind of visions that Macron has been espousing.

In one of her first speeches on the subject she all but laid out a point-by-point rebuttal of Macron's plan. "European centralism, European statism, communitising debt and Europeanising social security systems and the minimum wage would be the wrong approach"—words she put to paper in an opinion piece published in Germany's major paper. The assertion is that individual nations should be protecting their individualism, their culture and most of all they need to protect their budgets. In the last 10 to 20 years, it seems that Germany is the European bank of last resort as it is continually asked to foot the bill for everything from a Greek bailout to stemming the tide of immigration. This has been a major issue for the more conservative elements of the CDU and their sister group in Bavaria. It has also been a major recruiting tool for the populist AfD party. There is a sense that any sort of European unity will simply mean more burdens heaped on Germany. There is little support for this now that the German economy has been slipping into growth of less than 1%.

The rest of Europe is essentially being asked to pick sides between France and Germany, but the reality is that until and unless these two nations agree on a plan, there will be very little progress in either direction. The populists are still influential in all the major EU states, but all have reached their natural boundaries as far as political influence is concerned. They are unlikely to rule unless as part of a broader coalition, but they are able to play the role of spoiler even when they are kept on the outside looking in—as has been the case in both France with the National Front and Germany with the AfD.

Brexit Vote Deadlocked

Tomorrow, the British Parliament is expected to hand Prime Minister Theresa May another resounding defeat on the issue of Brexit. The plan seems doomed as even her office is talking about this rejection as a certainty. The deal that she struck with the EU has not changed despite all the controversy as there has simply been no wiggle room from Europe. The two sides in the U.K. are not budging either. Those that are anti-Brexit are as determined as ever to get another chance at the polls, while the pro-Brexit forces are just as determined to keep the U.K. at arm's length from Europe.

Analysis: Up until recently, the impact of Brexit was somewhat abstract to the average British voter, but there have been economic cracks showing up virtually every week. The consensus view is that GDP growth will collapse. The population is now starting to see price hikes on imported goods and lower wages. The pattern is recessionary and there is not much the U.K. can do about it. Granted, Europe is not faring all that well either, but if anything, the Europeans are more determined than ever to hold their ground. The fear in the EU is that other nations will choose to split from the EU if they think they can command a better deal. The leaders in Italy and Greece have already made suggestions that they would be better off alone. The U.K. is going to have to be the one that budges, but at this stage there is no path to that position that seems feasible. It is not clear that the Europeans would let the U.K. back in.

A Little Something for Everyone

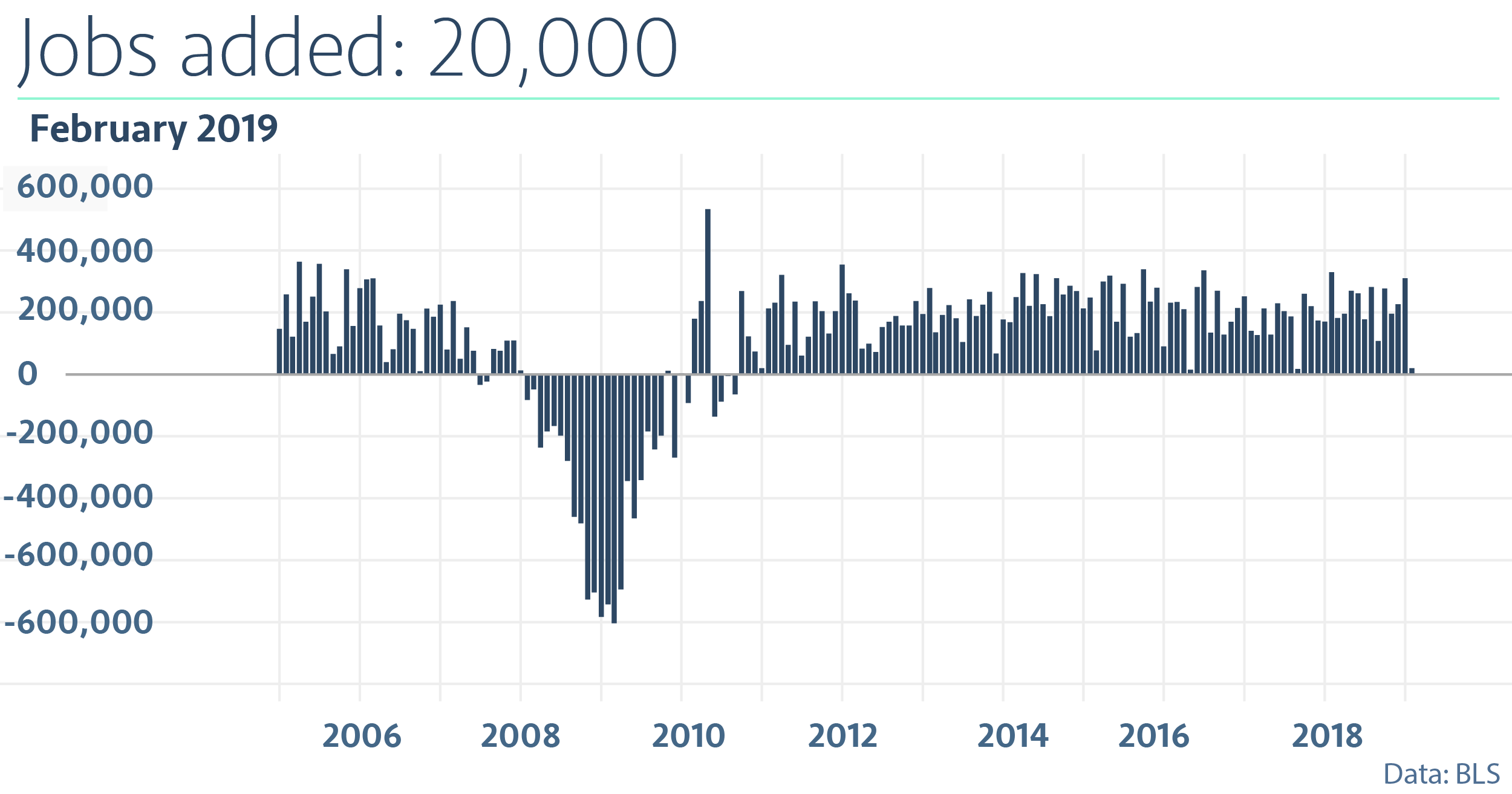

Are you a glass half empty kind of person? The jobs report released March 8 showed a very anemic gain of some 20,000 jobs when the expectation was for a gain of around 180,000. Or, are you more the glass half full type? Then you can note that the overall unemployment rate fell to 3.8% and the gains in wages were the most robust in close to a decade. Maybe you are more like my engineer father who simply observed that one had insufficient liquid for the vessel in question. Then you would note all the elements that would make this month's readings a little unusual. This was, for example, the first full month of employment data since the government shutdown. This was also a very cold period of time. Frigid temperatures can really mess with everything from construction to manufacturing to retail. Is there anything that can be definitely said about this month's jobs numbers? Yes. Much can be gleaned from the details.

Analysis: The overarching good news is there has continued to be job growth—especially when one looks at the three-month moving average. It has been 186,000; quite consistent with the pace of growth through the bulk of the last few years of economic recovery. This pace is nothing to dismiss as there have been some major hurdles to overcome in the process. Hiring is simply not that easy at the moment—even for the companies that are ready, willing and able. There are over one million more jobs on offer than there are people looking for work. Those who are currently seeking employment may lack the skills or education needed for these jobs. We have been harping on the job shortage issue for years. This is just another manifestation. The hiring that took place over the last several months has been marked by the willingness of employers to hire those that are less than ideal candidates. They will require training. That much is certain. A bigger issue is they are among the last to be employed in the U.S., which puts their willingness to stay hired in some doubt. There are many reasons people would still be seeking work after years of abundant job opportunities. Some have only recently been laid off, others have been in parts of the country with little job opportunity, but there are also those who have been content without a formal job as they made a living with part-time work or off-book work or various kinds of government assistance.

Wages are finally starting to respond in the way the Philips Curve suggests. This concept dates back to the 1950s. Its basic premise has been that when the unemployment rate is very low, there will be higher rates of wage-driven inflation as it is assumed that people will be asking for and getting higher wages because employers compete for their services. Add in the fact that a significant number of states and cities have been raising their minimum wages and the expectation was for significantly higher rates of wage inflation. Thus far, this has not been true. The wages have yet to rise to that level, but they are finally heading that way. As they rise, there will be more concern regarding future inflation. This kind of inflation can move very quickly as wage hikes tend to trigger several more. That has been the problem with increasing the minimum wage. It is not that some of the lower-paid people are getting a better deal. It is that the guy who once earned twice the minimum wage is now making the same as the new hire and demands that his/her status move accordingly with a wage of $30 an hour. Companies can't afford the cascade of wage hikes, but failure to keep pace means risking the loss of these experienced employees—especially when there is a low level of joblessness.

The good news is that job growth is still taking place. That has not been the case for many of the other industrial nations. Employment has leveled off in Europe (albeit at a lower rate than was the case a couple of years ago). Japan has seen a decline in hiring and even China has been slipping. It has been harder to hire than ever. Employers have been tapping into new sources of labor—everybody from the newly retired to those convicted of crimes. The only source that has slowed down has been hiring from other countries.

Differing Opinions as Far as Growth Is Concerned

The annual ritual of a presidential budget has begun. This is always an exercise in politics more than one rooted in economics or even fiscal policy. The White House budget is advisory as the decisions on what to spend and how to raise revenue will come from Congress. When President Trump was presiding over a Senate and House that were both in the hands of the GOP he had a little more control, but even in those years, his priorities were not always those of his own party. Now he has opposition from the Democrats who control the House and many of his plans will be modified or ignored.

Analysis: Perhaps the most fundamental position taken by Trump and his advisors is that growth rates this year and next will be roughly the same as they were in 2018. That means growing at over 3%. The assertion is that continued reduction of regulation and the continued influence of the tax cut will be enough to drive growth. This is not a position shared by many economists. The majority assert that growth rates will fall back to the previous norm of around 2.5%. This is not bad growth for an economy as large and mature as the U.S., however. At 2.5%, the U.S. will sport the fastest growth of any of the industrial nations—Europe will be struggling to maintain 1% growth and Japan may fall below 1%. The point is that 2.5% growth is not fast enough to sustain all the spending called for in the 2019 White House budget. That means an expanded deficit and debt. The debt is already more that 100% of the nation's GDP and the deficit is almost at 4.5% of that GDP. These are unprecedented levels for a nation not at war or facing some other national calamity. It costs a great deal to service that burgeoning debt.

A Most Important Concert

I confess to some bias here as I am convinced that every concert put on by the Liberty Community Chorus is important. It is an opportunity to hear the dulcet tones of my lovely wife and about a hundred of her closest friends. That said, there are concerts that stand out. The upcoming concert is one of them—especially these days. The theme is "You Are My Witnesses: A Holocaust Remembrance." This is a concert that was staged before and was one of the most powerful performances they have presented. The pieces are alternately joyous and somber, a combination of honoring the dead and damaged while acknowledging the bravery and self-sacrifice of millions of people.

Job Performance

Job performance since the recession has been somewhat volatile from one month to the next, but it has been essentially consistent. The U.S. economy needs to add between 200,000 and 300,000 each month to keep pace with population growth and the number of retirements. In contrast, the Chinese economy is faced with adding between 1.3 million and 1.4 million.