Strategic Global Intelligence Brief for December 3, 2019

By Chris Kuehl, Ph.D., NACM Economist—

Short Items of Interest—U.S. Economy—

Services Domination Shrinks—

The U.S. has long run a deficit when it comes to goods. The fact is U.S. consumers want low prices and lots of variety and have long availed themselves of the global output. At the same time, the U.S. has run a surplus with almost every nation when it comes to services. Throughout the world, it has been U.S. accountants, lawyers, bankers, marketers and so on that have dominated. That position has been eroding over the last few years as global economies have slowed and as trade tensions have taken a toll on the reputation of the U.S. There has also been growth of the service sector in nations that once employed U.S. companies almost exclusively.

Fed Reviews Inflation Policy

The current Fed policy holds that the rate of inflation should not be allowed to exceed 2%. That has been the view for the last few decades. The current rate is not close to that limit, but there are signs that wage inflation is starting to kick in as there was a 3% increase in wages in the last labor report. There has not been much movement as far as commodity costs are concerned, but that can change fast. The Fed has now suggested that a rate above 2% would be tolerated if the move was slow and there was no real threat of a runaway inflationary period. In other words, there is concern over the threat of deflation as well as inflation.

Have the Tariffs Helped?

When the tariffs were imposed on nations importing steel and aluminum to the U.S., the primary goal was the protection of the domestic sector. The hope was this would help rebuild the economies in the industrial states. The impact has been hard to assess, which illustrates how complex this kind of policy can be. It certainly helped U.S. producers compete against the cheap imports, but the tariff and trade wars have resulted in a drastic slowdown in the global economy. The loss of momentum globally has meant a significant drop in demand for steel and aluminum from the U.S., or anywhere else for that matter. That has limited the positive impact on the "rust belt" states.

Short Items of Interest—Global Economy

Green Finance

The statements from the head of the European Central Bank (ECB), Cristine Lagarde, are being hailed in some quarters and roundly condemned in others. A number of institutions in Europe and elsewhere are adding the issue of climate change to their criteria for action. Now, so is the ECB. The idea is to make dealing with climate change a key part of discussions regarding interest rates and monetary policy, but at this stage it is unclear just what this means. The banks fear that those who assert they are doing something to match the green initiative will be allowed greater risk tolerance. Few have any idea what compliance with these goals will require. It feels more like a public relations gambit than anything solid at this point.

Conservative Gains in the U.K.

The polls have been pointing to a strong showing by the Tories in the coming election—even as the voters are voicing objections to the Brexit plan. It seems that the vote is not exclusively about Brexit. The attacks by a recently released terrorist have pushed that issue to the forefront. The early release policy was implemented by the Labor Party, but there have been 10 years during which the Tories could have changed it. Now this has become part of Prime Minister Boris Johnson's stump speech, shifting more support his way.

Collapsing Governments in Europe

In just the last few weeks, there have been several governments falling apart as everything from scandal to coalition disagreements take their toll. The prime minister of Malta resigned over accusations of a coverup of the murder of a prominent journalist and critic. The prime minister of Finland has been forced out as the coalition splintered over reaction to a postal strike. The government in Spain has not been able to form because the coalition partners can't find common ground. The voter in Europe remains angry and disgruntled.

Yet Another Trade War in the Offing

As President Trump arrives in Europe for the NATO meetings, the mood is a mixture of anger, frustration and confusion. It has long perplexed the European nations that Trump has been so hostile to the organization the U.S. essentially founded some 70 years ago. Granted, the focus of NATO shifted dramatically with the end of the USSR, but threats remain to the U.S. and Europe from Putin's Russia, from wars in the Middle East and terrorism. The last time NATO rallied around its alliance was on the day after 9/11 when Article 5 was invoked on behalf of the U.S. This is why operations in Afghanistan have been NATO-led in many cases. At the start of the Trump administration, it was thought there would be close relations between the U.S. and France as well as with the U.K. There is no longer any such illusion. The rhetoric coming from the White House makes it clear Trump sees Europe as a rival at best and in most senses, it is treated as an enemy.

Analysis: The latest round of trade hostility involves France as Trump has promised a massive set of punitive tariffs on a wide range of French goods—everything from wine and cheese to consumer goods and a whole host of industrial goods that are widely used in the U.S. manufacturing sector. The issue is the new French tax on digital services. The tax will hit U.S. companies such as Apple and Alphabet. This has been deemed unacceptable by Trump despite the fact that countries regularly tax the operations of foreign companies. The U.S. has been taxing this way for decades. It is hard to understand the motivation on either economic or policy grounds; that leaves a more personal motivation.

At the start of Trump's term, it seemed a relationship might develop between the two new leaders. Both Trump and French President Emmanuel Macron were political outsiders who came to power due to voter frustration with the status quo. Neither had held elected office before and championed big changes. The first summit meetings between the two were full of handshakes and smiles. This soon faded as Macron was unable to bring Trump around on issues of climate change, trade or the U.S. role in the Middle East. The rapport has now become real animus as Macron has become the champion of the EU and Trump has become a major critic of all things European. The public statements from Trump have been insulting and directly aimed at Macron who has responded in kind. The proposed trade war is just an extension of this mutual hostility.

There was an assumption at one point that Trump's trade policy was calculated and intended to level the playing field. It was considered a tactic. Many analysts assumed that once some trade breakthroughs were accomplished, the trade wars would be called off in order to boost the U.S. economy. It is now clear this is not the plan. The U.S. economy is stuttering due to the trade war—exports are way down and the economy has become utterly dependent on the consumer. Still there has been no give in the trade war as these battles have now become a war of wills between Trump and various world leaders.

NATO Claims

The animus towards NATO has been hard to fathom, but it has become more intense with every year of the Trump presidency. The latest point of contention has been the claim by Trump that his pressure has been responsible for the increased spending by NATO members on their mutual defense. The organization now requires that members spend at least 2% of their GDP on defense. Most of these nations spend far more than this directly and indirectly with the largest countries spending the most. The decision to require 2% spending was made in the aftermath of the 9/11 attacks and therefore happened during the Obama administration. There has been no appreciable increase in spending during Trump's term. As a matter of fact, there has been a reduction in actual outlay as NATO troops have been pulled out of Afghanistan.

Analysis: The prime focus for NATO has been global terrorism since the attacks on the U.S., U.K., France and other member states. For the most part, the NATO troops and resources have been at the disposal of the U.S. command. The one area of contention between the U.S. and NATO has been Russia. The Putin regime has been seen by NATO members as a direct threat. There have been attempts to oppose Russian moves in Ukraine and other regions. There has also been tension between NATO and Turkey. In both of these situations, the Trump policy has been at odds with NATO strategy.

Lots of Data to Peruse This Week

After the deluge of food over the last week, we now get a veritable cornucopia of data. The highlight of this week's number feast will be the various editions of the Purchasing Managers' Index (PMI). Monday, featured the manufacturing version of the index from the Institute for Supply Management and on Wednesday, it will release the latest version of the service index. This week will also feature index numbers from Germany, China, Japan and many others. There are a couple of factors that make the PMI such a useful tool for keeping score. Perhaps the most important is that it is unbiased. Purchasing managers are not in a position to fudge the data—they are merely reporting whether they bought more of something, less of something or they bought the same amount as last month. By tallying up all these inputs, it is possible to get an accurate read on business activity without the concerns that accompany a lot of the other surveys. For example, the surveys that are connected to consumers rely on that consumer offering their opinion accurately—not something that always happens. The PMI is also current as these are inputs from this last 30-day period. Finally, there is the ease of understanding that comes with the diffusion index that states that anything over 50 is expansion and anything under 50 signals contraction. This system has inspired a wide variety of index offerings—including the Credit Managers' Index we interpret for the National Association of Credit Management.

Analysis: The U.S. version of the PMI remained in contraction territory, but improved a little from where it stood a month ago. The sense is manufacturing may finally be stabilizing a little. For the past year, the index has been steadily faltering as U.S. manufacturing has been forced to contend with the challenges of the trade war as well as the slowing of consumer activity in some key sectors. The sales of vehicles have been sluggish, farm machinery sales are courting recession, the oil sector has slowed as demand globally has ebbed and so on. The service index is expected to be stronger, but there are some worries about the strength of the U.S. service economy going forward.

The data coming from Germany and Japan is not expected to brighten anybody's day. German data showed a nice surge in September, but that is not expected to have carried through into October. Industrial numbers will reflect the fact Germany has been badly hurt by the global economic slowdown and the various trade wars that affect an economy that is over 55% dependent on those exports. Japan has likewise been hit by the slowdown in China due to the trade war. There is also the additional complication of a trade war between Japan and South Korea.

Good News Expected on the Jobs Front

This time of year can be a little challenging as far as tracking the unemployment situation as there is a great deal more temporary hiring taking place. The two sectors that add lots of people are retail and transportation with the latter responsible for the largest numbers of new hires. In another month or so, they will be gone. A further complication is that roughly 40% of those taking these holiday positions are already full-time workers in another job. The data this week is expected to be positive and reassuring to the Fed and investors in general.

Analysis: The expectation is there will an additional 180,000 to 190,000 employees added and the jobless rate will likely remain at 3.6%. The really good news is that wages may be growing at a 3% rate. That would be close to the pace that would trigger some wage inflation. Not that inflation is a good thing, but for the bulk of this recovery period, the inflation rate has been so low that many have been worried more about deflation and stagnation. A healthy dose of wage and salary boosts would propel the economy back to solid 2% to 2.5% growth.

Retail Surges

The whole month of November has now been transformed into "Blackvember" as the retailers seek to get hold of that early consumer spend, but that does not mean Black Friday and Cyber Monday have lost their cache. Both of these traditional days for deals and spending set records this year as the retail community saved their best opportunities for this traditional time period.

Analysis: That Black Friday set records is not surprising given the fact it is a holiday for most people so they can go out and do their shopping. Cyber Monday was a thing a decade ago as most people had faster access to online shopping at work and thus did their cruising for deals once the break was over. Now they can shop online from anywhere, but the day has been an excuse for retailers to add yet another special day for deals.

The expectation is that sales will now slow for the next few weeks. The procrastinators will ramp up the week prior to the arrival of the holiday. Most of them will be men with little idea of what they should be doing. This will lead to the last big surge for the retailers—return season. It is estimated that roughly a third of what men get at the last minute will be returned. When the recipient brings this stuff back, they are not in the best of moods and therefore tend to spend twice to three times as much as the original gift cost as a means to express their attitude to the original attempt.

The Joys of Maintenance

I have reached the age when one's body starts to resemble a house. I know that as a homeowner I have to be prepared for the unexpected failure on occasion. The water heater goes bad, roofs need to be replaced, sinks leak and so on. I was not necessarily ready to face the organic version of all this. You are reading today's edition of the newsletter a day late as I needed to get a review of my retinal surgery from a year or so ago. All is as desired, but the day was spent with eyes so dilated work was impossible. Fortunately, my current "house" has passed all the inspections, but the process can be annoying. There is a lot of routine maintenance required these days and recovery from unusual efforts generally takes two to three times longer than in past years.

This was the weekend for putting up holiday décor (in between the other required duties). By the end of the day, my muscles were demanding to know just why I felt the need to get off the couch—after all, there are still plenty of Hallmark movies to catch up on. There is one window in particular that looms menacingly as I need to employ the "big ladder." This monster is heavy; each year I am convinced I will slip and put it through the house. I managed to get the garland and wreaths up with no crisis—now I just have to get them down next year (and I might wait until May). There are still some minor touches to add, but the bulk of the festooning is over. This year we will be visited by our three great-grandchildren from Florida, so I have an excuse for all this tacky yard art—other than the fact that I am still basically a child.

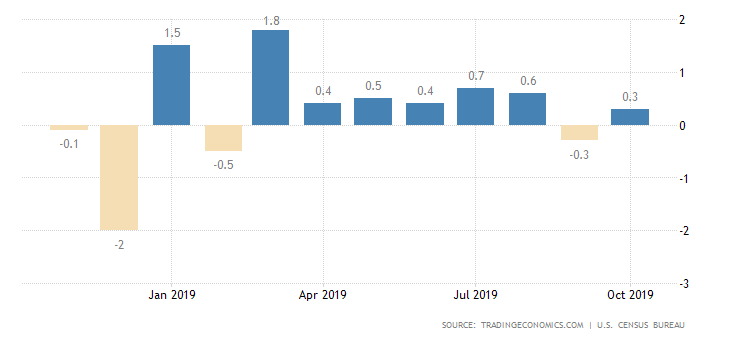

U.S. Pattern of Retail Activity

The pattern of retail activity in the U.S. has been stronger than expected for much of the year. This has been attributed primarily to stability in the job market. As long as people are confident in their ability to stay employed, they are willing to spend their paychecks and access their credit. The one cautionary note thus far this year is that big ticket purchases are down as compared to past years. The majority of the spending has been on items that cost $200 or less; there have been fewer purchases of cars and expensive items.