Strategic Global Intelligence Brief for April 3, 2020

By Chris Kuehl, Ph.D., NACM Economist—

Short Items of Interest—US Economy—

Massive Job Loss

As expected, the job numbers look really bad—a loss of over 700,000 and this is not even counting the numbers that occurred in the last week. This is certainly stunning but totally predictable. There are, however, still considerations that make this situation far less threatening than under normal circumstances. This was an imposed recession—jobs cut because government mandates have forced companies to close. Presumably, the majority of these jobs return when the restrictions are lifted. The critical question is when. Do these restrictions end in May or June or later? Do consumers return to their normal patterns right away or will they continue to be concerned and reluctant to return to old habits.

The Home vs. the Away

There are many divides as far as the workforce is concerned. There are the gaps by educational level and the gaps by skill level. There are gender gaps, racial gaps, age gaps and others. Now there is the gap between those who can work at home and those who can't. The home worker is using technology and has a job that does not require being at the workplace, but many do not have that luxury. They are suffering a much bigger loss. They either have to stop going to work altogether, or they run the risks that we have all been asked to avoid. The manufacturing sector is part of this population, but so are most of the service sectors as these people can't avoid being in contact with others.

Tracking

One of the techniques that has been employed by other nations has not been considered an option in the U.S. up to this point. South Korea, Singapore and parts of China have used tracking technology to see where infected people might have been and where at-risk people might be found. They have been using the GPS function on phones primarily. It has been used as a way to determine who might have been most at risk. This has been an unpopular concept in the U.S. and in Europe as it implies too much government intervention. On the other hand, it has been helpful as far as monitoring the spread of the disease.

Short Items of Interest—Global Economy

Asian Recovery?

The latest data from the Purchasing Managers' Index readings for Asia are perhaps the best news heard in a while. China has jumped back above the 50 line (expansion) after falling into the contraction zone in the low 40s. There has been progress in South Korea, Japan and Singapore as well. The numbers continue to be awful in Europe and in the U.S., but there is some hope that eventually the Asian pattern will manifest elsewhere.

Singapore Deals with Re-infections

The second wave of virus outbreaks have affected Singapore as people have been traveling back to the country from other parts of the region. Many of those who have come back to Singapore came from infected parts of China and India. Now, the country is attempting to close its borders more completely. There have also been more school closures and some re-imposed restrictions. Since the pandemic is global, it makes the risk from migration very significant. The sense is Singapore had turned a corner, but the threat has not vanished. The hope is that swift action will once again reduce the incidence and threat.

Speeding Up Vaccines

The race is on to develop a vaccine. The makers are now urging regulators to speed the process up dramatically. This carries a certain amount of risk as there are many cases in the past where the vaccine proved to be deadly in its own right. The German researchers assert they could have a vaccine in months if they are able to bypass some of the regulation and testing. The situation is one of gauging urgency and threat.

Possible Truce in Oil War?

The oil war launched by Russia and Saudi Arabia has been flying under the radar to some degree as the world has been focused on the COVID-19 issue. The governments in these two nations have deliberately engaged in a strategy designed to cripple oil production in the U.S. The rise of the U.S. as a major oil producer has been swift as the oil shale revolution evolved. It was just a decade ago that the U.S. imported 65% of the crude oil needed by U.S. refineries. Today, the U.S. is an oil exporter and has even sent crude to Saudi Arabia at intervals. The U.S. no longer buys much from the OPEC nations and clearly competes with these nations. That has prompted them to engage in strategies designed to win back market share. This is the kind of behavior one would expect from any company or sector. The actions taken lately, however, have gone beyond seeking competitive advantage. In most respects, the actions of Russia, Saudi Arabia and some of the other OPEC nations would quality as dumping as they are selling oil at a price less than is profitable.

Analysis: The decision to expand production at the same time that prices were cut resulted in a drastic reduction in the per barrel price of oil. The fall has been to less than $20 a barrel, considerably less than the minimum needed for the U.S. to make money. The oil producers in the U.S. need prices of at least $50 a barrel, while Saudi Arabia can manage some profits at $25. Russia really can't make money at less than $40, so they are clearly dumping their oil on the market. In the last day, there has been a slight hike in the price of oil as there have been assertions by Trump that a deal will be reached with both Saudi Arabia and Russia. The problem is neither of these nations has confirmed that any such deal is in the works. In fact, the Putin regime has been emphatic as it asserts it will not alter itss strategy.

The rapid drop in demand has added to the crisis as the global shutdowns crush economies all over the world. Even without the actions of these oil producers, there would have been a decline in the price of oil simply due to the sharp reduction in consumption. The oil producers in the U.S. are now demanding a reaction to this attack. They are requesting sanctions be imposed against those nations that are under pricing their oil. They want the U.S. to end its imports of oil from Saudi Arabia. For the most part, the U.S. imports from other nations to feed refineries on the East Coast as there are few pipelines that connect the middle of the country to these facilities. That makes it cheaper to get oil by tanker from the Middle East, Latin America and Africa.

European Economic Collapse Accelerates

As expected, the data from the Purchasing Managers' Index (PMI) throughout Europe is sending a desperate signal. These are the worst numbers seen since the surveys started—exceeding the declines that were experienced during the 2008 recession. The composite score for the eurozone went from 51.6 to 29.7. Given that anything under 50 indicates contraction, this reading is brutal in the extreme. Almost every economy in Europe registered the worst numbers seen in years—Germany, France, Italy, Spain—all seeing numbers in the low 30s and even 20s. The issue in Europe is the same as it is in the U.S. The moves to isolate and contain the spread of the virus have meant a massive shutdown of economic activity. That has plunged the entire region into a swift crisis. Unemployment rates are surging and have been exceeding 30% in the hardest-hit nations.

Analysis: As with every other nation coping with the virus, the economic crisis has been self-inflicted. The business community has been mandated to shut down. That means a reversal of that shutdown order would allow for a recovery, but only if some conditions are met. If the consumer is not willing to resume old habits, there will be no demand to rehire people. Those who have lost their jobs will not be in a position to do much spending for a while—even if they get those jobs back soon. There are also many businesses in Europe that will not be able to survive a shutdown that lasts more than another month.

An extremely tough decision will have to be made and soon. The virus will not be eliminated completely until there are effective treatments and cures and until there is a vaccine. That could be many months away; the global economy will not survive that long. There will have to be a decision to restart the business community even as the virus threat still exists. The tradeoff will be very difficult as a determination will have to be made that additional infections will be tolerated. The more pressing concern is that consumers will remain fearful even if the restrictions are lifted. That will prevent them from boosting the economy. Plans to revive the European economy are under review, but there has been no consensus whatsoever.

Too Little and Too Late

At the moment, the entire reaction to the COVID-19 threat has been reactive. The crisis is immediate and demands action if there is to be an end to the medical and economic impact. At the same time, there is a need to identify what could have been done to prevent this situation from reaching this point. This is vital if the infection is not to become an annual event. Thus far, it has been made abundantly clear the U.S. and most of Europe reacted extremely slowly and failed to take the steps required to ameliorate the impact. Those nations that responded quickly and decisively seem to have made progress and may be able to declare success in dealing with the outbreak within the next week or so. It is not that these countries have been immune to the spread of the virus, but they have experienced less damage and may be experiencing recovery sooner than later. Is their strategy something others can emulate?

Analysis: The bottom line is that coping with the COVID-19 outbreak requires action in four areas. There has to be a level of isolation for those who are vulnerable to the disease as well as those who have been exposed to the virus. The second requirement is an adequate supply of equipment to treat those who have the disease as well as testing procedures. The third requirement is sufficient capacity to survive the economic impact that stems from the isolation efforts. The fourth requirement is development of effective cures, treatments and a vaccine. The U.S. and most of Europe has failed in all four of these areas as reactions were too slow.

The isolation demands didn't develop until the disease had spread widely—even today, the majority of the country is not practicing any sort of isolation or containment. In nations that seemed to get a handle on this more quickly, there were swift efforts to isolate the vulnerable and to reduce the levels of exposure. The U.S. is still unable to test even a fraction of the population—at last count there have been around 60 tests per million people as compared to 3,800 tests per million in South Korea and 3,200 per million in China. The health care infrastructure has been utterly overwhelmed and now lacks adequate supplies of everything from respirators to protective gowns. The inability to test those in the health care system has meant that many are getting sick, which creates another shortage. It is not that any nation was completely prepared for this outbreak, but countries that had experience with outbreaks of viruses such as SARS, MERS, swine flu, avian flu and the like were far better prepared for COVID-19 given that experience.

The economic impact has been extreme; there has been little or no preparation for this. There had to be an understanding that shutting down tens of thousands of businesses would create an instant employment crisis and would immediately put these businesses in crisis. There was no move by the government to deal with the economic impact for weeks after the decision to shut down. The steps to protect the economy should have been taking place at the same time as the shutdown, but instead, the reaction was delayed by weeks. The help from the $2 trillion bailout will not be generally available for another few weeks at the earliest.

Finally, there is effort to find treatment options as well as a vaccine. This is not something that can be rushed given the fact the disease is new. The race to find a cure and a vaccine is on and there are efforts all over the world. The reality is that nobody yet knows what the timeline will be—past experience has shown that breakthroughs are sometimes very swift and sometimes are very slow to emerge.

The lesson learned from this is that reactions to future threats must be much faster and be more decisive. The actions to deal with this outbreak have been chaotic and politicized to the extreme. This should not have been this damaging. Intense scrutiny regarding what to do in the future will need to become a priority. The U.S. now accounts for 40% of the rise of COVID-19 cases globally.

Miserable Employment Numbers

At the time of this writing, the latest employment numbers had not been released, but there is no mystery as to what they will indicate. It has already been revealed that that some six million people have filed for unemployment. The expectation is that job losses will be severe and the rate of unemployment will be very high. As crushing as this is to the economy, it could be highly temporary.

Analysis: Everything depends on timing at this stage. The employment crisis has been imposed by government action—not any sort of traditional economic issue. People did not lose their jobs because there was a lack of consumer demand. They did not lose their jobs because their employers were unable to compete and were forced to go out of business. The jobs lost have been overwhelmingly in sectors that have been shut down by mandate. This means that the majority of these jobs return the moment the restrictions are lifted—at least that is the hope.

In addition to the lifting of the restrictions there will need to be a consumer reaction and here is where timing matters. If the restrictions extend beyond the end of April, there is a risk the consumer will sink into a deeper funk and remain skeptical regarding recovery from the virus. That would mean people would be slow to resume old habits. If people do not return to the restaurants, sporting events and airline flights, etc., the need to hire will be diminished. In addition to this consumer behavior, there is the ability to survive a month of shutdown. It has been estimated that around 10% of small businesses in the locations affected by shutdowns will not survive the month of April. If the shutdowns extend into May, the failure rate will likely jump to 25% or higher. This would mean a significant number of the lost jobs would not return. The hope is that restrictions are lifted or relaxed in the next three to four weeks and consumers return to old patterns. These are both possible, but there is also the distinct possibility that neither of these positive developments occur.

How to Help Small Business

The grim reality is that small business will take the biggest hit from all this—even if there is a recovery of some kind in May or June. The larger operations will feel this decline, but they will have more access to resources and reserves when the crisis starts to fade. The small business is a lot like the general population in that it lives from paycheck to paycheck. Is there much we can do for that sector? In truth, our options are limited, but they exist.

Shop local with a vengeance. If one has the opportunity to buy from a small operation, that should be the first choice—even though they might not have the lowest prices. Obviously, those that are now financially strapped will be limited, but anybody with discretionary income should try to steer towards the local option. Everything from take-out at the local eatery to shopping at the local grocer.

The second issue is responding as quickly as one can when the crisis starts to fade. When these places open up again, they will need all the patrons they can get and fast. We will still be in cautious mode, but those fears will have to be managed. Finally, we need to look for opportunities to promote and support once things return to some semblance of normal. That means becoming aggressive marketers and promoters of our favorite haunts so people know these businesses are back.

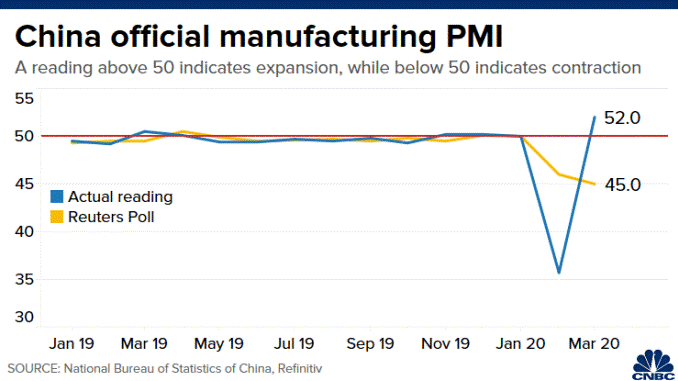

China's Official Manufacturing PMI

The latest numbers from the Purchasing Managers' Index are miserable—for the U.S. as well as just about everybody else. That is no shock, but if one wants to take heart to some degree, there is the performance of the Chinese PMI. This is a classic "V" recession indicator—at least at this point.