By Chris Kuehl, Ph.D., NACM Economist—

Short Items of Interest—U.S. Economy—

Decent News Expected from Durable Goods Data

By the time you read this the Commerce Department will have released the latest durable goods numbers. Most expect them to show another month of improvement—even as the aerospace sector continues to grapple with the issues surrounding Boeing. The data last month rose by 2% over the previous month due to a recovery in some of the aviation sector, but even without the activity in aerospace, there was a gain of 1.7%. The expectation for this month's reading is a hike of 1.1%—not quite as robust as previously, but still respectable. At some point, the woes that have sidelined Boeing will come to an end and it is expected there will be a lot of catching up.

Report on Consumer Activity Due

There will be lots of attention focused on the data released by the Commerce Department on Friday, Aug. 30. There will be new data on both consumer spending and consumer income. These have become all-important pieces of data. The manufacturing sector has been taking its lumps of late. That has heaped even more pressure on the consumer. The growth in both income and spending has been solid—reflecting the overall health of the employment sector. As long as people's jobs are secure, they are satisfied enough to keep buying things and services. That drives the economy in lieu of a stronger manufacturing sector. The expectation is that personal income will rise by 0.3% and expenditures will be up by 0.5%.

Decidedly Mixed Messages

It has been nearly impossible to write anything that accurately describes the state of negotiations between the U.S. and China. The range of remarks in just the last 24 hours has been extreme. Trump essentially declared a full-on trade war and demanded that U.S. companies pull out of China. However, within hours, he stated China had reached out to start new trade talks (which China denies). Trump indicated he had second thoughts and the markets rallied. Then, Trump stated he wished he had been tougher on China sooner and he will not back down. Does anybody have any idea what the plan is? It seems not.

Short Items of Interest—Global Economy

U.K.-U.S. Deal in the Offing?

There has been a lot of backtracking of late. British Prime Minister Boris Johnson has been taking a tough stance on Brexit and has asserted he can get the Europeans to bend. They deny this. Johnson had been countering this position with the assurance that a deal would be worked out between the U.S. and U.K. that would solve all of Britain's ills. He has been tempering these expectations of late and has now stated getting that deal will be hard as the U.S. will have to make a lot of concessions. These demands have been met with a cold response from Trump. Suddenly, this trade deal seems a lot more distant than it had been.

German Business Confidence Falls

The level of confidence among German businesspeople and investors has now fallen to a seven-year low. The consensus view is the U.K. and U.S. are locked into policies that will erode the global economy and Germany will suffer the consequences. The primary strength of the German economy has traditionally been its export prowess. The exports from Germany make up more than 50% of the national GDP. The trade war between the U.S. and China, the Brexit pull out and the general slowdown in the global economy is hammering the Germans hard. The business community is expecting things to worsen in the coming year.

Hong Kong Riots Escalate

The demonstrators began to throw Molotov cocktails as well as bricks at the police and the authorities responded with the deployment of water cannons. This caused a retreat of the protestors but certainly not capitulation. The conflict still seems to be marching to an inevitable and bloody conclusion.

Disastrous G-7 Meeting

It is safe to say the U.S. has never been as isolated from its allies as it is now. President Trump has never really cared what other world leaders thought of him or his policies, but he did go through the diplomatic motions. The latest G-7 meeting was tense and unsettling from the very start as there was nothing the other members could agree on regarding Trump and the actions of the U.S. on a host of foreign policy issues. The attempt by Trump to put a positive spin on the meetings failed utterly as the leaders of the other six openly challenged his interpretations and asserted the U.S. was completely out of sync with everyone else. Even erstwhile ally Prime Minister Boris Johnson from the U.K. was somewhat critical of Trump and seemed less than convinced that Trump would come through with some promises made to the U.K. Needless to say, this set of meetings rattled markets all over the world. The consensus view is the U.S. and China are now officially in a bitter trade war, one that will likely accelerate the advance of a global recession. The G-7 group was once seen as a stalwart U.S. alliance—far more supportive of U.S. goals than the more diverse G-20. It is no longer. The members include the U.K., U.S., France, Germany, Italy, Canada and Japan—the seven-largest industrial economies in the world.

Analysis: There were many issues brought forward. The U.S. was at odds with the other members on all of them, but three stood out as the most serious and responsible for the biggest rifts. The top of the list was the ongoing trade war with China. This confrontation has escalated to the point of no return and the impact on the global economy has been profound. The previous incarnation of this policy could be interpreted as hardball negotiating, but it has now become an open confrontation that leaves no room for a reduction in tension as both sides have taken steps that will be nearly impossible to back down from. The position of the Chinese has become abundantly clear—they are now waiting to see if Trump remains in office past next year. They fully expect 2020 to feature a very bitter and all-out set of confrontations. The Trump position is just as rigid with demands that U.S. companies leave China. Statements to the contrary, Trump does not have the power to enforce this order. The U.S. is not a state-run economy and government does not have the ability to determine where and how a business operates, but there are many ways a business can be affected by the demands of the sitting regime. There are programs in place to encourage business and there are regulations that can make doing business far harder. There is now considerable concern that the Trump administration will try to make dealing with China more difficult. To put it bluntly and simply—a trade war of this magnitude between the two-largest economies in the world will create the conditions for a true global recession. That is exactly what has been predicted by most governments and international organizations.

The second major point of contention was Iran. The U.S. position has been to put intense pressure on the Iranian regime with an eye to forcing some kind of regime change. There is no longer even an attempt to negotiate with the Iranian government as the U.S. is convinced that exerting this kind of pressure will provoke a revolution in Iran that overthrows the current theocracy. Nothing in the behavior of the Iranian populace supports this notion as even those seeking reform in Iran are blaming the U.S. for all of the problems in the country. The French tried to provoke a dialogue by inviting the Iranian foreign minister to the meetings, but there was no contact with the U.S. or Trump. The position of the other G-7 nations is opposed to that of the U.S. It seems likely that plans to subvert the U.S. plan will go forward despite threats of retaliation from the U.S. through yet another round of tariffs.

The third area was the Amazon. The G-7 nations are critically concerned about the policies of President Bolsonaro's regime in Brazil. The Amazon has been set ablaze by illegal farming operations that want to replace the forests with crops. The value of the Amazon as a carbon sink and producer of oxygen is unparalleled. Its destruction is extremely detrimental to the rest of the world. The members united in a strong condemnation of the burning, but Trump did not support the demands. He has become close to Bolsonaro who has referred to himself as the "Tropical Trump."

The U.S. has rarely been this isolated from its ostensible allies. The leaders that once tried to develop a relationship with him are now quite definitely members of the opposition. There has never been a relationship between Trump and Chancellor Angela Merkel of Germany or Prime Minister Justin Trudeau of Canada, but President Emmanuel Macron of France and Prime Minister Shinzo Abe of Japan tried in the past to build some rapport. That effort has ceased and even Prime Minister Boris Johnson has been hedging his bets as he waits to see if Trump will make good on his promises of a big trade deal with the U.K.

Shifting Positions

The G-7 meetings were as tense as they could be, but even as they were winding down, the statements from Trump were changing. The bellicose approach to China and the imminent trade war was replaced with comments suggesting a "second guess." China responded to the onslaught of threats with an offer to open talks again. Trump suggested he would be open to that—just hours after declaring his intent to ban U.S. companies from doing business in China.

Analysis: The bottom line is that nobody has any idea what the policy of the U.S. is. The battles between the members of Trump's advisory team have become public; nobody really knows who is in charge from one day to the next.

Global Bankers are Depressed

The drama of the G-7 meetings has had a miserable impact on the meeting of the world's central bankers in Wyoming. These annual get-togethers in Jackson Hole are usually somewhat staid affairs with the various central bankers discussing the tweaks and adjustments they are capable of making, but this year has been much different as most of the speeches have had an edge of desperation.

Analysis: The bottom line they assert is that politics and the trade war are creating havoc in the global economy that they will not be able to offset with the tools at their disposal. Lowering rates when they are already at record lows will not be as stimulative as many in politics seem to assume. They are also very worried about the attacks on the Fed by Trump. The rhetoric and threats issued by Trump are generally heard from various autocrats in less developed nations—not in the U.S. The Fed has not buckled under this pressure, but it complicates their ability to influence policy.

Global Generation Gap

It has become almost impossible to attend any sort of management meeting without hearing a speaker or two or three comment on the differences between the generations—Boomers, Gen-X, Millennials and now Gen-Z. These differences affect how people expect to be managed, their business loyalties, their consumer preferences, their ambitions and their personal actions. Increasingly, the issues are extending to political preferences. This has become a focus for the U.S. and for many other nations—even those that do not sport much of a tradition of democracy.

Analysis: Few nations spend as much energy assessing the mood of the population as does the U.S. There are new opinion polls released almost hourly. This pace will surely accelerate as the 2020 elections draw closer. The divide between the Millennial and the Boomer is as wide as it has been in many years and will play a major role in the coming elections. That same divide is appearing in other nations. The young population is far more interested in the populist parties in Europe—both from the right and left. Many of the Brexiters are young and young voters have flocked to parties such as the Alternative for Germany, the National Front in France, the Five Star Movement in Italy and others. At the same time, the left-leaning parties have grown—Greens, Socialists and parties that focus on race and gender politics.

In the U.S., there are major divides over patriotism, religion and child rearing. Over 80% of Boomers place patriotism as very important while about 65% of Gen-Xers are so inclined. Only around 40% of Millennials do, which is less than half the number of Boomers. On religion—around 65% of Boomers think it is very important, Gen-Xers come in at 45% and Millennials at around 30%. The attitude towards having children differs as well—55% of Boomers think it is important, around 44% of Gen-Xers think it is and only 33% of Millennials do. Given that the Millennials are in the prime years for starting a family, this does not bode well for the future of the workforce.

There are areas where the gap between generations is not as great. All cohorts seem to value hard work (over 80%), but the Gen-Xers are more committed to the idea than either of the other two. Community involvement is high on everybody's list (between 55% and 70%) with the Gen-Xers at the high end and Boomers at the low end. The issue of tolerance is high for all three cohorts (around 80%), but highest among Millennials.

The political issues that matter differ as well. The Boomer is far more likely to list security concerns as top of mind as well as economic issues. There is concern about terrorism and the potential for either recession or inflation. The hot button issues of race, culture and immigration are important as well. Generally speaking, this group supports the basic structure of the economic system, but has chafed at tax decisions and worries more about debt and deficit than the others. Gen-Xers are far more concerned about the state of the debt and deficit as they expect that to impact their retirement planning. They are worried about health care (along with the Boomers) and have some of the same concerns over cultural issues, but not to the same degree as Boomers.

The Millennial is often in stark contrast to the other two. There is not nearly the same support for the current economic system which many judge as fundamentally unfair. There is far more interest in cultural issues such as racism and gender discrimination. There is not the same level of opposition to immigration and far more interest in global issues such as climate change. There is general disenchantment with current politics, which may affect decisions to be made next year. The level of disenchantment with politicians is high. That applies to those on the left and right.

A Wedding!

This weekend was highly unusual and far more exciting than is normally the case. My oldest grandson got married! He is the large animal veterinarian who against all odds found his true love. He never had any challenges getting female attention as he is tall, blond and quite good looking (if I do say so myself). His problem was that his profession takes center stage in his life—always. Most of the girls simply didn't get this and relationships didn't go anywhere. Then came his new wife. She is a country girl straight out of central casting. She is tall, blond, blue-eyed and utterly at home with the livestock that makes up his world. Her family was in the dairy business most of her life and now her father runs several hundred head of beef cattle on 2400 acres. As they dated, most of their time together was on his farm calls. There has rarely been a more well-matched couple.

The wedding was simple but thoroughly enjoyable. My wife's contribution was making the wedding cake—a three-tiered monster that had her stressed out for weeks. The two-hour drive to the venue with the cake in the back was nerve wracking, but it made it unscathed. The couple found it to be just what they wanted. On top of its good looks it was very tasty! The ceremony was delightful. Even the rain stopped so the whole thing could be held outdoors as they wanted.

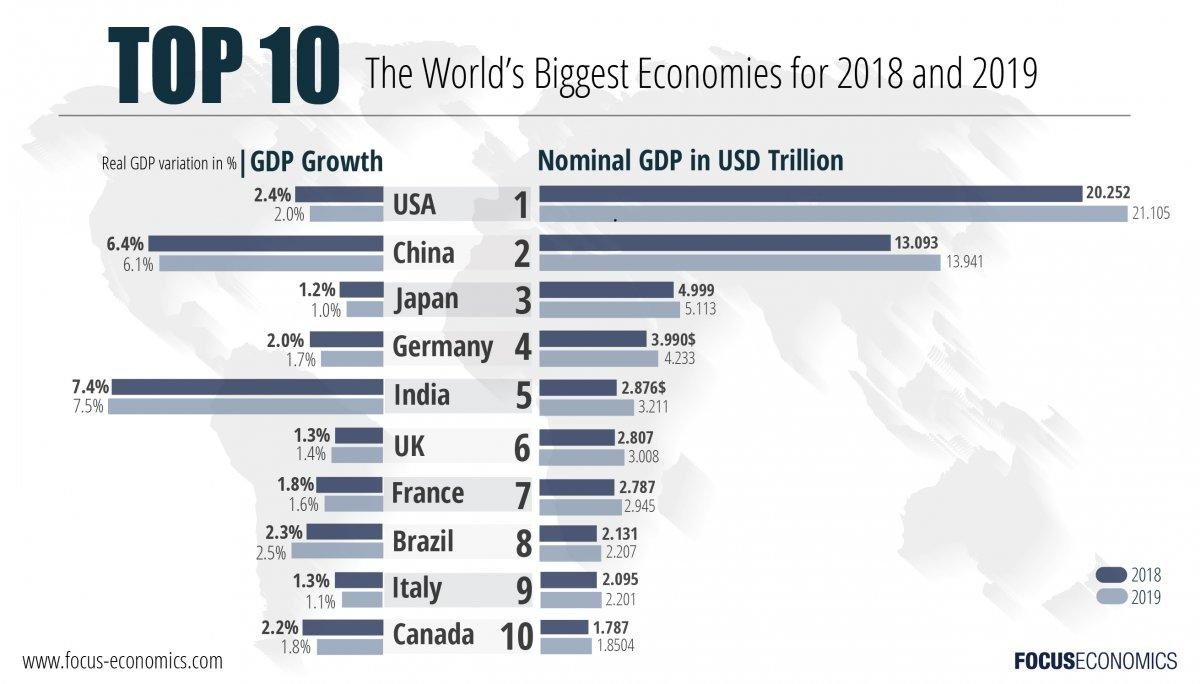

The World's Biggest Economies

As important as the G-7 economies are to the world—this is no longer the group that entirely dominates the global economy. As the chart shows—China, India and Brazil are all ranked ahead of Italy and Canada. The notion is that G-7 meetings are for the industrialized and democratic states. That would provide an excuse to keep China off the list. India and Brazil are both clearly industrialized and democratic and would seem to warrant a place in this panoply.