Strategic Global Intelligence Brief for September 6, 2019

By Chris Kuehl, Ph.D., NACM Economist—

Short Items of Interest—U.S. Economy—

Job Growth a Little Disappointing—

It wasn't a bad jobs report, but it wasn't a great one either. The expectation had been there would be another 160,000 to 180,000 jobs added, but the reported number was just 130,000. This is not bad; however, this is the time of year that job gains traditionally start to accelerate. There are all the people starting in school systems all over the country—teachers, support people and the like. This is the time retailers start to beef up their staff in anticipation of the holiday as well, although that hiring is more intense later into September and October. The transportation companies and warehouses start to staff up, but that also gets more intense later in the season. This addition of 130,000 is OK, but reports suggest companies have become generally more cautious about expanding as they look at the impact of the trade war.

Fed Starts to Talk Up Next Rate Reduction

It appears the Federal Reserve is prepared to lower rates another quarter point. This is not a universally supported position within the Fed's Open Market Committee nor among the rest of the regional Fed leaders. It is likely that both Esther George and Eric Rosengren will dissent again. They may even be joined by others. The challenge for Fed Chair Jerome Powell is to communicate that these reductions are not a response to pressure from Trump. Powell has carefully outlined the rationale for this cut—the struggles of the global economy and the impact of the trade war. He has also been trying to control expectations by pointing out that rates are already very low.

Vagaries of the Job Market

There are good jobs that pay well and have a future and there are fast-growing job markets, but the occupations in each category differ dramatically. The fastest-growing segments of the job market are almost entirely in the low-paid service sectors. These include everything from food workers to those providing personal care to the elderly. Even the majority of new businesses are low-revenue service companies such as coffee shops, lawn care and the like. The good jobs are in health care and tech, but they require extensive education and experience. The sweet spot in terms of good pay and availability is in skilled trades, but these require training as well.

Short Items of Interest—Global Economy

Johnson Gets Slammed

There were two key votes that would set up U.K. Prime Minister Boris Johnson's plan and he has lost both of them. He had attempted to shut down Parliament for a period and force a new election, but that effort was thwarted in Parliament as much of his own party defected. His plan to force a no-deal Brexit also lost. Now, the U.K. will work to start up negotiations with the European Union (EU). Johnson has been PM for only a few weeks and is already essentially a lame duck. The new election would likely have strengthened Johnson's position given how unpopular the opposition leader Jeremy Corbyn is, but now he faces a Parliament he can't control as too many of his own party have turned on him.

Vietnam Promises More Imports

The nation that has benefited most from the trade war between the U.S. and China has been Vietnam as the U.S. has increased the level of imports from that nation by over 65%. The government in Vietnam is now assuring the U.S. that it plans to buy far more from the U.S. so it is not seen as profiteering. The Trump team has not yet attacked Vietnam, but there have been criticisms of other nations which have seen stepped up exports.

Race for IMF Head

It now seems more likely that Kristalina Georgieva from Bulgaria will be the next head of the International Monetary Fund (IMF). The rules that imposed age limits on the candidates has been waived. She is 66 and the rules stated that nobody over the age of 65 could run. At the same time, some of the other candidates have taken their names off the list. Her elevation has been hailed by Europeans as well as the developing nations, but the U.S. has been lukewarm at best.

If the Economy Does Slow Down—What Will Be the Reason?

To begin with, there is no guarantee the U.S. economy will slump or head into an actual recession. The signs of late have been decidedly mixed with something for the glass-half-full and the glass-half-empty crowd. The latest data sets are feeding a little more nervousness, but at the same time, there have been encouraging signals. The real question is what would actually trigger a real slowdown and perhaps a recession. There are always the unexpected shocks to the system that can batter an economy, but the U.S. is large enough that it can withstand things like natural disasters and even wars. It usually takes a series of events that affect the confidence and ultimately the performance of the consumer and the business community. At this juncture, it seems there are three real threats to the continued growth of the economy. In order of likelihood and impact these would be: the trade war, shifts in the workforce and the impact of global economic slowdown.

Analysis: The most obvious drag on the economy is the trade war. Tariffs are a tax and taxes do not stimulate growth no matter how they are described or justified. The consumer is paying more for the things they buy and will end up forking over an extra $1,000 to $3,000 a year due to the tariffs imposed on goods from China. If there was just a tariff war with China, the impact might be slightly less dramatic, but there have been tariffs imposed on most of the U.S. trade partners and even more threatened. Canada, Mexico, India, Europe and nearly everybody else that sells to the U.S. has had to face some kind of tariff imposition. Collectively, this adds up to as much as $5,000 to $8,000 in additional costs to consumers. Much was made of the tax cut in 2018, but this reduction has been dwarfed by the tariff imposition. At this point, many of these tariffs have been removed or reduced, but nobody is sure whether they will be returned at some point. That creates downward pressure on the economy as well. There is no doubt the U.S. has become too dependent on China and no doubt that China has not been playing by the rules of global commerce. It may be necessary to undergo this economic pain, but there should be no illusions that this strategy will not negatively impact the U.S. economy. It is very likely the trade war alone will peel as much as a point from GDP growth. That takes the U.S. into territory that is close to recession.

The second threat is a complex one. There is a transition underway in the labor force, and most of the change is far from positive. There is the long-standing issue of labor shortage. In many key areas of the economy, there are far too few qualified people available to fill positions. This shortage has been affecting manufacturing, construction, transportation and health care for years. Now, there are shortages in high tech and the professions like law, accounting and finance. Much has been made of the low rate of joblessness and all the job creation, but the vast majority of the new jobs created have been in the low-paid service sector. A big reason there has been job growth is that there have been thousands of retirements—10,000 Boomers become eligible for retirement every day. That amounts to some 3.5 million a year. The effort to replace them has been the biggest motivation for a low level of unemployment, but the new workers are not as skilled as those they are replacing and they are not getting paid as much. The large number of retired people means that there are only 2.9 working people for every retired person. By 2030, it will have dropped to two workers per retired person. The U.S. needs a bigger workforce and it needs one immediately. Unfortunately, the current attitude towards immigration is as bad as it has been in decades. Foreign workers find it very hard to gain access to the U.S. Too few workers and workers with bad jobs that don't pay well creates a slowing economy.

The third issue is somewhat related to the first. The global economy is in some trouble—that much is patently obvious. Germany is already in recession, which in turn, drags the whole of Europe down. The Brexit chaos is sending the U.K. into a full-on depression that will last for years. Japan is stagnant and has been for decades. China is close to recession level; Mexico is on the brink of recession and will soon be joined by Brazil and Argentina. The last man standing is the U.S. It is not possible to continue growth while the rest of the world collapses. Granted, the U.S. is not as dependent on exports as Germany—they rely on exports for 55% of their GDP. But the U.S. depends on the global market for 15%, a higher percentage than in Japan. The U.S. sells everything from agricultural output to highly sophisticated machinery and needs those foreign markets.

Can Oil Epicenter Shift?

There are few sectors that have seen as much volatility as has the oil sector. If one looks back to the predictions made by oil analysts just a few years ago, it would seem the world was on the brink of true economic ruin. The assertion was that oil would be selling at between $120 and $150 a barrel, that the pump price would be closing in on $6 a gallon; outright shortages would be common. The power of OPEC would have amplified to the point that Middle Eastern politics would be altered forever. Russia would become a dominant world player again on the strength of their oil position. All of this emphasis on oil and the high costs would provoke a massive investment in all manner of alternative fuel—natural gas power, hydrogen power, ubiquitous electric vehicles, drastic expansion of mass transit. Very little of that prediction has come to pass as the per barrel price of oil has tumbled as low as the mid-40s and is now struggling to get to $60. The power of OPEC and Russia has been blunted and most of the oil-producing region of the Middle East is in chaos. The urgency to develop alternatives has all but vanished; many of these new technologies have been abandoned altogether.

Analysis: The primary reason for all this change has been the development of the oil business in the U.S. The promise of oil production in the Dakotas, Wyoming and Texas was finally fulfilled. The U.S. went from being a nation that imported over 65% of the oil it needed to a nation that exports crude and only imports when the price is right. This is not the only factor that has altered the oil landscape; there are many more influencers developing. There is also a distinct global slowdown underway. This has already reduced demand all over the world. That is the main reason oil prices have not reacted to all the geopolitical turmoil that has affected oil producing states such as Iran, Libya, Iraq, Venezuela and others.

There are more big changes on the way, and perhaps sooner than expected. The oil business in the U.S. is booming, but that obscures the fragility of this sector. The fracking business is not cheap and requires per barrel oil prices to be in the neighborhood of $80—preferably at between $90 and $100. The forecast for the price per barrel is nowhere near this level. That has many of the U.S. oil producers in a quandary. Do they continue to produce or wait for that price to increase? The Middle East is not stable and hasn't been for years. This has been overlooked to some degree, but only out of necessity. The desire has been to replace this region as a source for the world's oil, but thus far, the alternatives have not panned out. The U.S. has altered the landscape, but most of the U.S. production has gone to the U.S. Global markets still seek an alternative to the volatility of the Middle East.

The region that could fill that need is Latin America, but this promise has gone unfulfilled for decades. Venezuela is in total shambles. Even if somehow Maduro could be driven out, it would take many years for the oil sector to recover. Neither Bolivia nor Ecuador has been able to develop as expected. Colombia has made strides since the defeat of the FARC insurgency, but is now contending with the massive wave of migrants streaming in from a shattered Venezuela. Brazil has thus far squandered its opportunity with endless corruption and exploitation and Argentina has been unable to get on track. None of these inhibitions are impossible to deal with, although the challenges are daunting. Should the political issues be dealt with, the oil sector in Latin America could easily supplant that of the Middle East and North Africa.

One More Thing—Commodities

There has been a factor in play for the last few years that has allowed the U.S. to skirt around some of the economic stressors. Commodity costs have been low and oil prices have sunk to levels nobody predicted even a year or so ago. The price of gas at the pump has fallen so low that the average driver is spending $1,000 less per year than they did two years ago. Metal prices have been down despite the tariffs on steel and aluminum. The price of lumber, cement, and many food commodities have fallen. Even the rare earth materials have been falling.

Analysis: How long can this be expected to last? Is there a big commodity price boost in the offing? In the short term, it seems unlikely as there is simply not enough demand to justify a big price hike. The challenge develops later as the producers of these commodities start to cut back on production. If demand is weak that is the logical thing to do, but at some point enough production will be pulled out of the system to create shortages. That is generally followed by price hikes which reflect that reduction of supply. It is not imminent, but it is inevitable. The real question for the future is how fast the producers can ramp up once there is a return to more traditional demand.

What Is This—Round 234?

It seems that hope springs eternal within the ranks of the investment community. Either that or they are engaged in a massive episode of self-delusion. There was yet another murmur from Trump that negotiations with China would resume and a corresponding murmur from China's President Xi. The markets surged and rejoiced as some assumed that cooler heads were prevailing. Never mind that neither negotiating team made any mention at all of a changed position or tactic or even a time for the talks to resume.

Analysis: The unfortunate fact is that neither Trump nor Xi really have much to gain from a resumption of talks—not unless the other side is prepared to totally capitulate. Trump can't sign off on a deal that allows Chinese exports at previous levels or that doesn't radically increase Chinese imports of U.S. goods. He gets far too much political mileage with his base from keeping China in the crosshairs. Xi has the same desire and issue. He can't afford to look weak and therefore will demand access to the U.S. market and will offer only vague assurances of access to Chinese markets. Politically, neither Trump nor Xi has been hurt by this confrontation and neither really cares what this does to their national economy—at least at this juncture.

We Are What We Watch

The advertising community is very savvy and sophisticated when it comes to targeting. The ads you see are designed to appeal to certain demographics. If you pay attention to them, you will know where you are supposed to fit. I do my best to skip through commercials and watch a certain amount of TV that comes without these ads. However, there are times they are unavoidable and I get some insight. I watch the local news a lot and have concluded that only the elderly and homeowners watch the news. Every ad seems to be for retirement homes, dentures, hospitals or alternately for siding, gutters, roofs, remodeling or yardwork. I caught a little bit of a football game last night and had to bail after deciding it was a boring defensive match. I was getting sick of ads that assumed I was a gluttonous drunk interested in nothing but trucks, gambling, booze and rude behavior.

I do have occasion to watch other shows. Even though I skip through the commercials, I am aware of them. Hallmark movies are peppered with ads for products that women would buy. The ads that accompany shows about zoos and vets feature travel opportunities and pet supplies. When one adds in the ads that appear through our social media interactions and internet use, one can figure out one's tribe pretty quickly. My challenge with some of these search-based-targeted ads is that they assume an abiding interest in the most casual of inquiries. Search just one time for a pergola kit and one will be forever the recipient of the latest pergola news. For the record, we gave up on that ambition in deference to my skill set when it comes to carpentry! If you know any pergola purveyors, would you kindly tell them to move on.

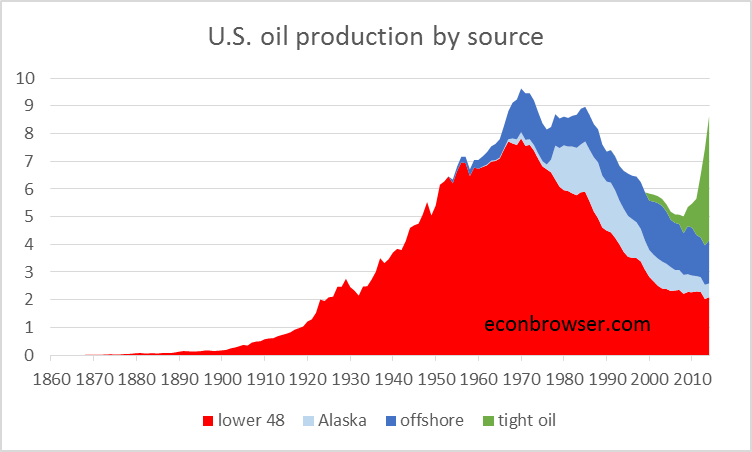

U.S. Oil Production by Source

Here's the story of U.S. oil in a nutshell. Peak production from the traditional areas in the U.S. was in the 1960s and then there was a swift decline. Oil from the offshore deposits also peaked in the 1970s and 80s and then started to fall off. The oil from the so-called "tight regions" only began to appear on the market in the last few years, but that is where all the growth has come from. It is important to recognize that even with the decline from the traditional sources, the total output is back to those peak years in the 60s and 70s.