Strategic Global Intelligence Brief for March 20, 2020

By Chris Kuehl, Ph.D., NACM Economist—

Short Items of Interest—US Economy—

Denial Always Helps

The latest statements from Trump and his team are anything but helpful and have added to the angst in the business community. States have been asked to withhold information regarding jobless claims. This is ostensibly to focus attention on the national numbers when it comes to jobless claims, but that will be intensely misleading. It is already very obvious that some states have been much harder hit by the pandemic than others. It is important to know what this has done to the economy of those states. The national numbers will be of very little assistance for several months as the states that have not been affected as much will obscure the impact on states that have a bigger issue

GOP Plan

The economic response to the virus outbreak has been a little slow to evolve, but it appears Congress is starting to get in gear and promises more to come. The plan that has emerged from the Senate is a combination of support for the health care community and some grand gestures that few analysts believe will have much impact. There are supposedly grants and loans on the way to small businesses and there will be tax cuts and delays. The move getting the most attention is the issuance of $1200 checks to people making less than $75,000 a year. This will have very little impact on those who are losing their jobs. It will also do little for the overall economy as consumers have been highly restricted in terms of their ability to consume.

More Bond Buys on the Way

The Federal Reserve has been employing as many of its traditional tools as it can in hopes that it calms the economy a bit, and especially the markets. The decision to lower rates to near zero was inevitable and so was the decision to buy more treasury bonds. A commitment to buy some $500 billion was made and the Fed has hinted that a larger purchase will be possible if the situation warrants. The central banks are waiting along with the rest of the world to see when this situation begins to improve. If the China experience of eventual control is matched by other nations, the efforts thus far may have been sufficient.

Short Items of Interest—Global Economy

Italy is Now the Epicenter

Italy has now surpassed China in terms of the seriousness of the crisis. There are more deaths and more infections, and the spread has not seemed to slow. There are two reasons the Italians have been hit so hard and so fast. The first is that Italy has the oldest population in Europe. That means a larger population of at-risk people. There is not much that can be done about this. The other issue is more salient. Italians have not accepted the restrictions. Reports indicate that life has been essentially as it has been with extensive social contact and almost no attention to the self-isolation protocols. There have been some communities that have complied and their infection rates have been far lower.

Back to 'Normal' in China

Volvo has closed its operations in Europe and the U.S. as a reaction to the spread of the virus, but this week they announced they are back to full operation in China. The assembly plant is back to work and so are the suppliers. The dealers are also back to work. Sales have been brisk, as Chinese consumers resume their old patterns. The world can only hope this is the model for the rest as that would mean normalcy in the next 30 to 90 days.

Oil Prices Crawl Back

The price per barrel of oil has crested back above $30 for the first time in weeks. The sense is that oil hit bottom a few days ago and will now start to find a more sustainable level. The problem is that for U.S. producers, the level needs to be somewhere north of $50 for production to be profitable. The sense is $50 a barrel oil is still a long way off.

Global Fed Reactions Calm Markets

The global nature of this financial crisis has demanded a truly global response. The world health authorities are doing their best to work with one another and find joint solutions. Now, so are the financial authorities. This is not as easy as it sounds in either situation. It is the natural response of a given government to take care of its own citizens before spending any time, effort or money on anybody else. The COVID-19 virus respects no borders and so has required a far more universal reaction. This has meant sharing medical resources and research. Now, it means sharing financial assistance and strategy. The U.S. and Europe have been at the forefront of this movement. China, Japan and South Korea have also become active in their cooperation. This stands in very sharp contrast to the actions of Russia. The Putin regime has chosen to play an intensely hostile role in every respect. There is the launching of an oil war designed to damage the U.S. oil business, there has been the deliberate spread of misinformation in Europe and the U.S. in order to create panic and there has been an outright refusal to provide any information regarding the spread of the virus in Russia.

Analysis: The latest moves from the Fed have been designed to stabilize the global economy as much as it has been designed to influence what is happening in the U.S. The Fed has agreed to provide billions of dollars in low interest loans to the world's other central banks as they struggle with balance of payments issues. The central banks outside the U.S. have to consider their hard currency balances as they attempt their own stimulus efforts. Most of them have been running very low on their supply of dollars. That would sharply curtail their ability to keep pace with the needs of their own economies. The Fed has essentially become the banker to the world.

This means that there is significant cooperation among central banks as far as preserving global liquidity. That has had a somewhat calming effect on the markets—at least for now. The challenge as far as bolstering the resilience of the global economy is that most of the stimulus efforts are unsuited to this kind of crisis. The trigger in past recessions has been lack of consumer and business confidence brought on by some kind of financial crisis or a drastic loss of demand. The solution was therefore to get more money in the hands of business and the consumer so demand would improve along with confidence. This time, the demand was strong enough and confidence was high enough, but suddenly the consumer was cut off from consumption. With the orders to remain at home, the level of consumption has utterly collapsed. That triggers other economically negative consequences as business starts to engage in massive layoffs.

Some Reasons to Remain Optimistic

The COVID-19 crisis has presented society with unprecedented strain. The aftereffects of this will be significant for years. Nobody is even sure what tone to take right now. In order for people to behave the way they must to halt the spread, they have to be scared enough to comply. On the other hand, too much panic results in destructive and downright stupid behavior. Amongst all the bad news there are some glimmers of hope.

Analysis: The best news is coming from China. This is the country that has been dealing with this longest and is therefore one to watch for what happens next. The data from Wuhan shows there has been a drastic reduction in the spread—no new cases for several days now. The research has also shown that mortality rates are lower than originally assumed—1.4% of those infected as compared to the 3.5% assumption earlier. The Chinese have shown there are effective drugs to treat the most seriously ill. The recovery rate for those who contract the disease is now well over 60%.

Japan has also developed effective treatments for the most seriously ill. South Korea has slowed the spread with a more cooperative population. They have not had to resort to the extremes that China has because the population has been willing to adhere to the recommended actions. That is a lesson the U.S., Italy and other nations have not learned.

Key to Economic Survival

In truth, there are many things that will have to happen if the global economy is going to get through this crisis. At the top of the list is preserving employment. This is not going to be easy as the economies of the world essentially shut down. Whole industry sectors have been affected (travel, entertainment, restaurants and the like). There is no way they can continue to employ people if they are basically out of business. It is now estimated the unemployment rate in the U.S. could reach as high as 20%—at least in the short term. The plans to send people checks will accomplish very little if these people have lost their jobs.

Analysis: There have been programs in some countries that tie government help to struggling business with their pledge to maintain employment. As long as these companies agree to hang on to their workforce, they get assistance. If they take that government aid and engage in actions such as stock buybacks, they lose that help. In many cases, a company will not be able to hang on to employees even with that assistance. Then, other steps have to be explored. The vast majority of companies have indicated they will bring those employees back as soon as they can resume normal business activity, but nobody knows when that will take place at this point.

California's Shutdown

There have been two basic schools of thought as far as containing the COVID-19 outbreak. The Chinese and South Korean governments made the decision to lock down the entire country and swiftly. The affected regions enforced what amounted to mass quarantine. The Italians, most of Europe and the U.S. preferred a plan that relied on voluntary action. Thus far, the Chinese approach seems to have worked and the U.S./Italian approach has failed.

Analysis: The decision to lock the entire state of California down was prompted by the fact that millions of residents have refused to cooperate with the health authorities. There has been little willingness to avoid crowds and little attention to restricting the spread of the virus. This is a nationwide issue as the behavior of the spring breakers demonstrates. The fact is the virus spreads quickly through contact. It is now clear the virus stays viable on various surfaces for hours. The refusal to self-monitor and self-isolate has left many governments with little choice but to enforce that isolation more aggressively. The problem is that societies such as in Italy and the U.S. and elsewhere in Europe are not as "cooperative" as those in many Asian states. These are not populations accustomed to the power of the police and military as are residents of China. The U.S. faces a grim choice—either a massive expansion of the virus or confrontations between the population and law enforcement.

When Does 'Normal' Return?

This is obviously the crucial question. The behavior of business, the investors and the consumer will depend entirely on how long this crisis lasts. The longer it drags on, the more severe the damage to the economy and the longer it will take to rebound. The primary challenge is that nobody has a solid response to that question of how long—there are far too many variables for a definitive response. At this point, there are three buckets as far as duration is concerned.

Analysis: The most optimistic assessment has the crisis fading by the end of May. This is based on the assumption that voluntary isolation will have limited the spread to a significant extent, but is mostly dependent on the behavior of the virus as the weather warms up. If the COVID-19 virus responds the way the flu virus has, it will not survive the warmer conditions. There are several studies under way to determine whether this warm weather response is significant. One of the distressing observations has been that COVID-19 is showing up in tropical countries at a much higher rate than expected. The self-isolation has been very spotty at best with most of the population in Europe and the U.S. ignoring the suggestions to stay home. A week or so ago, this assessment was considered the most likely, but now it has perhaps a 30% chance of developing.

The second bucket asserts the virus will not be under control until the end of the summer or later and that it will require truly draconian steps to achieve that level of control. The decision will have to be made that people are incapable of taking this threat seriously and will have to be forced to comply. Assuming that whole nations go on lockdown, the assertion is that the spread of the virus will be contained to the point it can be coped with. That doesn't mean that life returns to normal as these severe restrictions would remain in place for months—perhaps to the end of the year. The probability for this scenario is now close to 40%.

The third bucket is grim indeed as it asserts that isolation will not work at all. The sense is that societies can't be shut down enough to halt a spread. That means it will not be controlled until there is a vaccine. The companion issue is how to treat the disease. Right now, there are few effective treatments, but there has been some progress in China and Japan as far using new drug cocktails. If these are more widely used, the fatality rate would presumably decline. The best estimate is that a vaccine is available in a year to 18 months. This means the virus spreads and impacts for nearly two years before it can be brought under control. That is also the optimistic timeline and assumes the virus doesn't mutate and defy the vaccine efforts. This alternative now has a 30% probability.

The economic impact will be significant but manageable with alternative one. The sense is that normal operations will resume quickly as the restrictions on society are lifted. There is even a sense that a boom might follow the bust as people hasten to go back to old patterns. If the second option develops, the economic impact will be serious as millions of people will have lost their jobs and millions of businesses will fail. This option ushers in a real and extended recession. If option three develops, the global economy falls into deep depression that could take years to escape from. Unemployment rates would likely reach 30% or higher and governments would be powerless to stop the decline.

Silver Linings

Threats such as these expose varying personalities. There are those who remain dismissive of the whole issue and have made no attempt to accommodate. They are going around rubbing every surface in sight. There are those who have reacted in a panic and are now living in a yurt in the middle of the woods surrounded by 200,000 rolls of toilet paper. The rest of us are seeking to make the best of this. I have observed three positives thus far.

The first is that people are reaching out to friends and family more consistently. Not that we ignored them before, but we were busier a week or so ago. Now, we have some time on our hands and feel the need to connect—even if we can't actually be closer than six feet from them. The second is that people are exercising their empathetic impulses more consistently. The fact is most of us are not high risk or even medium risk. If we are infected, 85% of us will get little more than a cold. That we are willing to engage in the "social distancing" and other steps shows that we are worried about those who are under threat. The third positive is perhaps a little wishful thinking on my part. It seems that people are thinking more about what they want and need from those that ostensibly govern. The powers that be have been failing us for a long time—the U.S. is not what it once was or could be. Our leaders should have been prepared for this and they should be far better at managing the crisis now. If we start demanding more, it would be a very good thing.

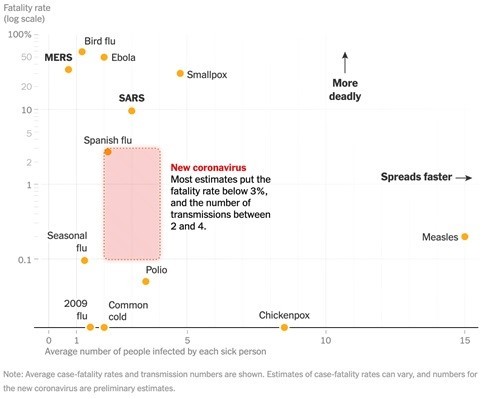

Infection Rates vs. Fatalities

This chart may bring a bit of clarity as far as the comparisons are concerned. The assumptions here were made prior to the latest study out of the Wuhan area that put fatality rates as low as 1.4%. That means COVID-19 fatality would be at the lower-left end of that box. This puts fatality rates near that of the flu, but it spreads faster. The facts show that SARS, MERS, Ebola, Bird Flu, Spanish Flu and smallpox are all deadlier, but only measles and chickenpox seem to spread faster.