Strategic Global Intelligence Brief for June 12, 2019

Short Items of Interest—U.S. Economy

Little Change in Inflation Threat

The latest Producer Price Index shows a very modest hike of 0.1%, essentially indicating there is no increase in underlying inflation to worry about for the time being. This has been one of the more baffling aspects of the economy of late as there really should have been some palpable threat of inflation by this point. The low rate of unemployment should have resulted in wage gains (at least according to the precepts of the Phillips Curve) and there should have been some pressure from commodity prices. That hasn't been the case. Expectations are that oil and metal prices will fall further as demand starts to erode. Only farm commodities are expected to go up in the months to come.

More Frustration With the Fed

Trump has not backed away from his attacks on Fed policy as he continues to assert rates are too high at 2.5%. The Fed itself has started to entertain the idea that rates will have to be reduced to keep growth going, but there is a major difference in terms of the rationale used by Trump and Powell. The Fed position is that trade wars, tariff wars and the slowdown in the global economy may be enough to pull U.S. growth down. Should that happen, the Fed will have to do its part to stimulate. At the same time, it will require action by Congress as far as fiscal policy is concerned—they will need to cut taxes or hike spending or both. Trump asserts the slowdown is all the fault of the Fed and these higher rates. Given that rates of 2.5% are historically low, this argument makes very little sense.

Historically Tight Labor Market

The gap between the number of jobs on offer and the number of people seeking work has never been wider. There is a massive shortage of workers. Finding people to employ now ranks as the No. 1 challenge for business—more concerning than taxes, regulation or any of the other traditional concerns. What is more worrying is that everything points to a worsening situation. Boomers are still retiring at the rate of 10,000 a day, legal immigration has dramatically slowed as would-be migrants fear a hostile reaction, skill gaps are wider than ever and the birth rate is lower than at any time in the last several decades.

Short Items of Interest—Global Economy

Bond Yields Plummet

The investment community is seriously worried about the future of global economic growth. That is propelling a massive shift into bonds. The German government is selling 10-year bonds with the lowest yield on record. The U.S. treasuries are also carrying very low yields. Despite this, the investor is seeking security in these government bonds as they sense that equity markets are headed for a major correction. The threat is real as these investor moods are often something of a self-fulfilling prophecy.

Hong Kong Protests Erupt Into Violence

The massive protests that have dominated Hong Kong for the last few weeks have now become violent as the local authorities have been trying to break up the demonstrations. The plan to allow people to be extradited to China for crimes that are not punishable in Hong Kong is seen as a move to destroy dissent and end Hong Kong's status as a semi-autonomous entity. The protests are a desperate attempt to resist the power of Beijing and could easily spin into a near civil war.

Mystery Surrounds Mexican Deal

One of the critical parts of the deal struck between the U.S. and Mexico was that the new National Guard would be deployed by Mexico to its southern border, some 6,000 troops. In fact, there is no National Guard yet—the first 1500 members are still in training. Furthermore, the unit was created to attack the drug gangs—not enforce the border.

Report from the Front

It is time for the index analysis we do for two manufacturing organizations: the Chemical Coaters Association International and the Industrial Heating Equipment Association. Both are heavily involved in sectors such as automotive, appliances, aerospace and anywhere else that requires the treatment of metal. Here is the executive summary and some excerpts from this month's analysis.

Analysis: There has been a mood shift—at least in some circles. Investors are driving bond yields down and the dreaded inverted yield curve now comes up in virtually every financial program. The basic economic facts remain solid, but trouble seems to lurk right around the corner. The latest jobs data was anemic with only 75,000 added, but at the same time, the unemployment rate stayed at 3.6%. The revised growth numbers for Q1 were down, but not by much. Despite the decent current situation, there is more trepidation about what is to come—the business cycle seems due to correct, but nobody is quite sure why. The most consistent fear is that trade wars and tariffs are taking a toll. Analysts suggested these moves could pull as much as a point off growth and now that seems likely—perhaps even this year. The index readings reflect this same set of concerns. Five of the eleven trended positive and six trended negative. The challenge is that the negatives mostly registered big falls, while the positives showed only modest improvement.

Sales of new automobiles and light trucks tracked down this month as they did last year. There have been several suggestions as to why. The consumer is weaker than has been the case earlier, but there has also been some impact from the tariffs and threatened barriers that would affect Europe. Another weak area was steel consumption. That would seem logical given the issues that have affected the automotive sector. This area has also been affected by the continued lack of investment into the public infrastructure. One of the biggest declines was in capacity utilization. Granted this category only fell by one point, but this is a sector where changes are generally subtle. The decline was the most precipitous seen in many months and comes as there had been hope for a trend in a more positive direction. The fact is companies are still trying to make efficient use of the machines they already bought. As with steel consumption, there has been an ongoing decline in metal prices. The simple fact is demand is not keeping pace with overproduction—partly a result of companies reacting to the potential for tariff-induced higher prices. There was a decline in both durable goods numbers as well as factory numbers, and the fall was significant. The consumer is cautious, which has meant more caution among producers. The usual impact of aerospace on durable goods has been blunted somewhat by the ongoing issues with Boeing's 737 Max.

Not all was gloom and doom, however, but the growth was marginal as compared to the more dramatic declines. Housing starts recovered a little, but this has been due to improvements in the stock market. Builders are favoring the upmarket projects. The motivation for that buyer is neither mortgage rates nor the cost of the house, but whether they made a lot of money in the market. The level of capital investment rose after a pretty dramatic drop, a trend everyone would like to see accelerate. The capacity utilization situation may prove to be a constraint, however. The rationale for more investment has started to fade due to all the angst within the investment community. The PMI New Orders index recovered a little, but is still far below what it was just a few months ago. That has been the same situation with the overall index as well as the employment and export sub-indices. The readings are all still in the expansion zone, but only slightly. It will not take much to drive these numbers towards contraction (a reading below 50). The Credit Managers' Index has been trending up for two months in a row now and that is solid news. The less exciting part of this data is that most of the gains have been in the service sector and not in manufacturing. The trend has been in the opposite direction as far as manufacturing is concerned. That will be a drag on the whole index. The transportation numbers look better than expected as trucking has managed to hold its own. The rail sector and ocean cargo are both feeling the pinch of the tariff and trade wars. Volumes of both inbound and outbound cargo have been falling and fast. The U.S. marked a low in both exports and imports last month.

New Automobile/Light Truck Sales

The data from the automotive sector has been slow to appear of late. This has created a delay in the latest numbers—perhaps there is reluctance to note the decline in sales that started to appear in the last few months. In truth, that is not really the motivation—rather it has been the unusual turmoil that has affected the auto sector lately. There have been threats to impose tariffs on European cars and car parts. That has cut into sales of vehicles from the likes of Volkswagen, BMW and Mercedes as potential buyers worry about access to parts down the road. There have also been threats to impose tariffs on Mexican goods coming into the U.S. Mexico supplies a lot of car parts as well as finished vehicles. Add in the trade tensions with Canada, Japan and South Korea and you have severe disruptions in the global auto sector. This is affecting sales as the consumer starts to worry. That is coming on top of a general sense of consumer slowdown across the board.

Metal Pricing

In most respects, metal prices are still down and falling. It is not too difficult to determine why. There has been a reduction in demand as manufacturing has started to slump. The tariffs and trade wars have taken a significant bite out of the pace of global growth. Nobody has a good feeling about imminent recovery. The producers have tended to react too slowly and have not slashed production to levels that this weak demand would seem to justify. It is expected global growth will stay on the weak side as Europe grows at less than 1% and China falls to 6%. The U.S. has been the sole engine, but is now showing signs of stuttering as well. Growth in the U.S. is falling back to norm—between 2% and 2.3%.

New Home Starts

The housing sector has been all over the place of late. One month it appears that the boom is well and truly over and the next month there is a tidy rebound. It is important to note that the new home sector is the smallest part of the total housing data. The majority of the buying and selling takes place in the existing home market. Here the data has been a bit more consistent. Sales of existing homes have been trending down for several months now, but new homes are responding to some additional economic factors. Traditionally, the most important determinants as far as people's willingness to buy homes are overall employment numbers and mortgage rates. If there is concern regarding job security, people are reluctant to buy homes. If mortgage rates are high, this will be an obvious deterrent. Lately, these have both been trending positively with jobless rates at record lows and mortgage rates starting to fall again. This opens the door to other influences—such as the behavior of the stock market. Many of the new homes being built are in the higher price range. Those that are in the market for such homes are not as affected by either jobless data or mortgages. They either have discretionary income to spend or they don't and the performance of the markets have provided a lot of people with that wherewithal.

Steel Consumption

The steel sector has been under a lot of stress throughout this year. The level of consumption has only been one area of concern. The imposition of tariffs has been little more than a political football. This has left the producers as confused as ever, not to mention their consumers. The original plan to impose tariffs on all imported steel was scrapped almost immediately as exemptions were handed out to all but a small collection of minor players (China, Russia, Turkey). Together, they accounted for less than 20% of all steel sent to the U.S. Then these exemptions were reneged upon, but only for a few months. Now Brazil and South Korea (number two and three importers into the U.S.) have exemptions. It has been promised that both Canada and Mexico (number one and four importers) will get exemptions as well. It has been next to impossible to predict demand and supply. The auto sector has slowed down, which has also affected demand, but a bigger issue is the lack of investment in the public infrastructure as this has traditionally been the most significant market for steel output.

Industrial Capacity Utilization

The drop in industrial capacity utilization has not been all that dramatic in terms of actual percentage as it has only declined from 78.5 to 77.9. The problem is that these numbers do not usually alter much and have hovered between 75% and 85% for many years. A slip of a full point is a big deal given that many thought they were seeing a pretty substantial rise in usage numbers prior to this collapse. The ideal percentage is between 80% and 85% as that signals there is little slack in the system while not suggesting that a period of shortage and bottlenecks would be imminent. It seems that many companies are holding off on acquiring new capacity—a signal that they are less confident of the future economy than they were earlier in the year. There is also a certain level of trepidation regarding the extra capacity they had been acquiring earlier. The reaction of many companies had been to buy product they thought might be affected by tariffs later in the year. That decision will have been a wise one if the tariffs take place, but if they don't, the decision may have been somewhat premature and there will be a struggle to figure out how to make that purchase productive.

PMI New Orders

The Purchasing Managers' Index (PMI) had been heading towards contraction territory and seemed poised to have lost all the major gains from the last year. The current numbers are stalled just short of that, but the margin is very narrow. It will not take much to plunge the readings under 50. The New Orders Index is the more forward looking of the Institute for Supply Management (ISM) readings. It is good news to see it rise back to 52.7 from 51.7, but this is not signaling a robust recovery by any stretch. The majority of the manufacturing community seems to be emphasizing caution above all else these days. That has been reflected in several of the ISM readings beyond the new orders data. Hiring is down and so are exports. The overall index has also slowed from what it was in previous months.

Capital Expenditure

The rebound in capital expenditure (capex) numbers was somewhat short lived but at least it has not totally reversed course. The connection between capacity utilization and capex remains strong and there is still more evidence that manufacturers are exercising a lot of caution when it comes to investment. A new wrinkle that may be playing a role is the possibility of a rate cut by the Federal Reserve. It was only a few months ago that such a development would have been considered a near impossibility. Today, the slowing economy has some in the Fed considering it. It is not that many companies are waiting strictly because they think a 2.5% rate might fall to 2.25%, but if waiting a few weeks might save some money—why not?

Can't Live With It—Can't Live Without It

Regular readers are well aware that I have a somewhat hostile relationship with modern technology. I am essentially a technophobe and maybe even a Luddite. I have only the dimmest understanding of how all this works, a source of endless frustration. This is largely because I am stuck between two worlds. I have friends that are immensely comfortable in the tech world. My daughter-in-law is a highly skilled systems administrator for crying out loud! From them, I get the pitying looks one gives a toddler trying to master shoe tying. On the other hand, I have friends who simply opted out of the whole thing and live happy and contented lives without iPhones, internet or anything else with more moving parts than a brick. I have no choice but to engage—my business demands it. So, I seek to enjoy the delights of Internet access and other miracles of electronic connectivity. The problem is that I have no idea what is going on.

As I started the day, I was informed there was an internet outage in my area. At least I was informed after connecting via my portable hotspot and searching Spectrum's website for 30 minutes. I received such useful pieces of information such as "Error Code IA01" and "reference ##$33455 %%$##." Do I call Spectrum and try to read that back to them using the Victor Borge technique of enunciating # and $ and %? Would it have been so hard to use actual English? Perhaps a phrase like "there has an outage been, fix it we will." Sit could have been something comprehensible to most of us and yet satisfying to the IT person's sensibilities. Absent any other remotely useful information, I will wait until something comes back to life. I am just grateful I know enough to have acquired an alternate connection to the internet.

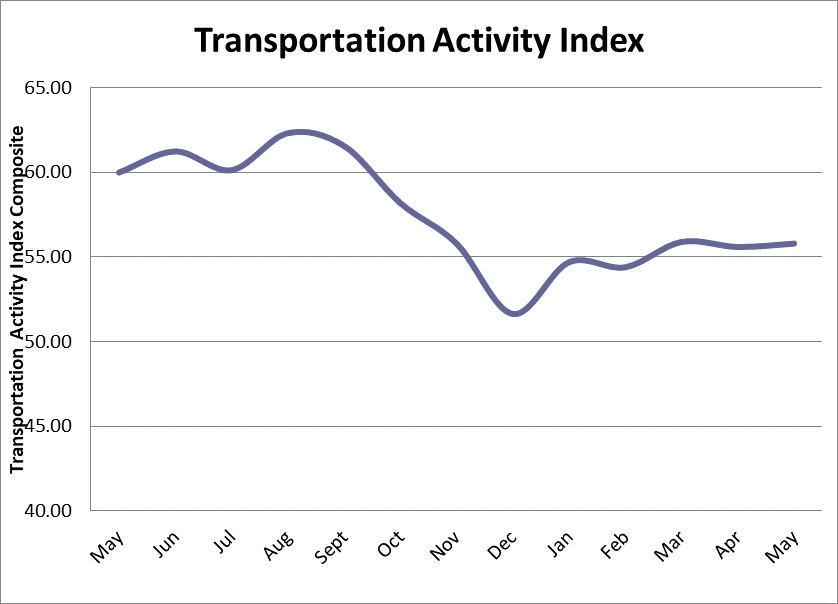

Transportation Activity Index

The Transportation Activity Index is a proprietary index designed by Armada to monitor the various modes of freight transportation as well as major inputs into that sector. The index has been a harbinger in more months than not—reflecting the role that transportation tends to play in the economy as a whole. The fact that this month's data is essentially flat is better news than some expected. The anticipation was that trends would worsen a little—especially in the trucking and ocean cargo arenas. In fact, ocean cargo was down as compared to last year, but inventory build in anticipation of tighter tariffs may still be taking place. The U.S. experienced a sharp drop in both exports and imports in the last month. That will likely be a theme for the rest of the year unless these tariff threats start to ease. Trucking is holding steady, but rail has been affected by the issues in farm country and the expectation of a bad harvest is worrying the sector.