Strategic Global Intelligence Brief for January 16, 2019

Short Items of Interest—U.S. Economy

Small Business and the Shutdown

Much of the attention has been focused on the estimated 800,000 people who are federal employees and not being paid. This will certainly have an economic impact in those regions where federal employment is a major part of the community, but an even bigger impact will be felt by the businesses that contract with the federal government. It is estimated that some 22,000 of them have been affected. Many are now forced to lay people off or otherwise find ways to cope with the lack of income. These are mostly small businesses that were deliberately recruited to do business with the U.S. as a means by which to encourage entrepreneurs. The next fear is that many of these companies will refuse to work with the government in the future due to lack of reliability.

Climate Change of Great Concern to Business

According to surveys from the World Economic Forum, the issue of climate change is now at the top of the list of factors to worry about in the future—at least as far as the corporate community is concerned. What is not clear is what to do about it. There is wide variation as far as finding solutions. About a third favor the lifestyle change approach of less driving and less activity that affects the carbon footprint. Another a third want emphasis on technological fixes and about a third want an emphasis on simply coping with the change and altering patterns to fit the new reality.

End of the Consumer Run

There is no doubt that 2018 was the year that consumers came back to life and resumed their old patterns. It was a very good retail season and consumers got busy with their credit cards again. The sense is that 2019 will not be the same kind of year as the headwinds are building. There are worries about the stock market, the shutdown, trade wars and so on. The signals of caution are appearing every day, but thus far, it is hard to tell if this is just the usual mid-winter slump or something more serious and lasting. There is agreement that much of what fueled the growth last year was the tax cut. That will not be repeated this year.

Short Items of Interest—Global Economy

Brexit Chaos

The Brexit plan that Prime Minister Theresa May has been trying to sell the British parliament has gone down in flames. That throws the entire debate into new territory. She has quite literally been caught between an immovable object and an irresistible force. The EU has pointedly refused to alter anything in the deal on the assumption that the U.K. would be strong-armed into accepting it. The anti-EU forces in the Conservative Party seem prepared to send the U.K. into recession rather than accept the deal as it stands. May is now suggesting that she may extend the deadline for the U.K.'s withdrawal past March 29 despite the fact this will infuriate the pro-Brexit forces in her party. The ball is really in the EU's court now as they will have to indicate a willingness to bend.

Massive Influx of Cash from Bank of China

The Bank of China has injected $84 billion into their economy in an effort to speed up the economy at a time when it has been slumping. The timing is significant as it comes at the Lunar New Year and is clearly aimed at the consumer. The hope is this money gets put to use soon and the retail and consumer sectors work to pull China away from its recent slowdown even as foreign exports decline.

Attack in Kenya

The attack on a hotel complex by members of the Al-Shabaab terror group out of Somalia has been put down and all the attackers killed. The terror group also killed 16 people and wounded dozens more. The attack on Kenya was the first in years and suggests that the Islamic terror group has started to move from its base in Somalia to other nearby targets. This hotel complex was full of foreign visitors and business people. It is an area close to where the same group attacked in 2013.

A Look at Some Index Readings

Each month, we put together a series of indices for two groups that are closely aligned with the industrial community: the Chemical Coaters Association International and the Industrial Heating Equipment Association. Both are engaged in treating metal for industrial purposes—everything from automotive to appliances and construction to aerospace. This is the executive summary of that report and a few excerpts from the body of the report.

Analysis: This is a month with something for both the optimist and the pessimist as there were five readings that trended positive and six that trended negative. What makes this month interesting is that these trends are closely grouped and related. Those readings that look mostly at the current economic situation remain positive as the momentum of 2018 seems to have carried into the new year, but the six that are not trending in the preferred direction all point towards the future. If we were to take just this month and extrapolate to the rest of the year, we would conclude that the time is now if you want to enjoy some growth as the prospects for more expansion are limited as the year progresses.

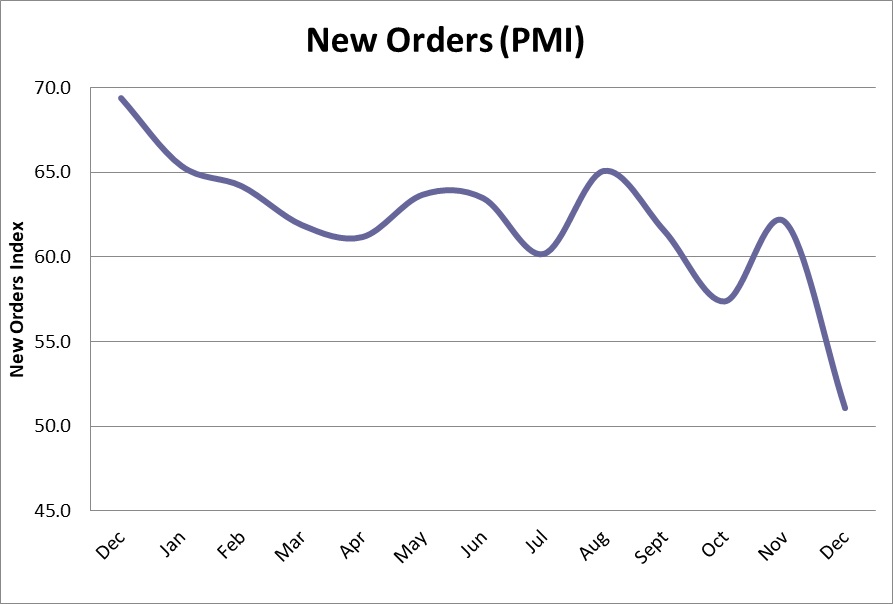

We will start with the things to keep you up at night. Three of these predictive readings really crashed hard this month. There was a very steep drop in the PMI New Orders index. It is now just barely above the line that separates growth from contraction. This is disturbing as the index was nearly at 70 just a few months ago. The overall PMI also fell, but not quite as steeply as this. That creates even more consternation. It suggests that companies are fearful regarding the future even as they continue to enjoy the current situation. This precipitous fall was also repeated in the Credit Managers' Index. What makes that data even more distressing is that most of the decline was in the favorable factors category—things like dollar collection, sales and amount of credit extended. The unfavorable factors weakened a little, but still managed to stay out of contraction territory. The third indicator that created a sense of unease was the Transportation Activity Index. This sector is often the harbinger of things to come. None of the sub-categories look good at this point. The expectation is that even FedEx and UPS will be reporting weaker earnings than expected—not a good sign.

The other three negative readings include the Sales of Light Trucks and Automobiles, Steel Consumption and Metal Prices. The decline in the automotive sector was extremely minor; the real surprise is that it is still doing as well as it is. Analysts had been asserting there would be a decline long before this, but the consumer can't seem to get enough as far as trucks, SUVS and CUVs are concerned. The steel data was more concerning as it had been expected that demand would hold given all the expansion in various industrial sectors, but the fact is that higher-priced steel and aluminum have hit demand to some degree. The fall in metal prices has been attributed to the same lack of expanded demand and some price hikes earlier in the year. Even the tariffs have not really driven aluminum prices that much higher.

The good news data is mostly the current data. It shows that 2018 growth started to carry forward into 2019. The New Home Starts data was better than most had expected and suggests there is still some life left in this market. It has helped that mortgage rates have been generally down and the price of a new home has eased in some parts of the country. There was good news as far as capacity utilization as well. The numbers are still just a little shy of that ideal position between 80% and 85%, but it is very close. Many sub-sectors have already entered that sweet spot. The capital expenditure numbers also improved, but not by all that much. The good news is that most companies seem to have integrated the equipment they bought earlier.

The data from the production side of the economy has been generally good. There were positive numbers in durable goods, factory goods and appliances. The durable goods data has not been affected much by the aerospace number as has often been the case, so this data reflects mostly growth areas in energy, health care and transportation. There was also some additional boost from construction-related equipment. The factory order numbers were high at the start of the holiday season as the retailers tried to gear up, but then fell off. Only recently have they seemed to recover some of their momentum.

New Automobile/Light Truck Sales

The vehicle market has been flat for a while now, but that trend tends to obscure some important developments as far as the overall market is concerned. The dramatic lack of demand for small cars has gutted that market. Carmakers are reacting with plant closures and shifts away from further production of these fuel-efficient vehicles—even the electric cars are taking a hit. The bottom line is that buyers liked nothing about the fuel-efficient car other than its fuel efficiency. The very second that gasoline prices started to trend down, the consumer could hardly wait to dump the small vehicle as they went back to bigger cars, SUVs and trucks. Once upon a time, there would have been a market for the smaller car among younger buyers as they would be attracted to the lower price, the lower cost of operation and the "greener" footprint. That younger buyer is not as prevalent as expected because they have options when it comes to transportation such as the ride share. The most consistent alternative to car ownership among young people has been Uber and Lyft. These options are expected to continue to grow. The bad news is that fewer cars are being sold. Thus there is reduced production, but the good news is that carmakers are building larger cars with lots more metal. The only growth as far as the car market has been concerned has been with trucks, SUVs and CUVs. The difference between the latter two is that an SUV is on a true truck platform and the CUV is on a car platform. It is really nothing more than an updated station wagon.

New Home Starts

The market remains generally down, but has started to show some signs of life in the last few months. As always, it is important to remind everyone of the housing market caveats—essentially that all real estate markets are local and that there can be huge differences in performance from one region to another. Nationally, there has been a little easing in terms of average home price and mortgage rates have come down a little. These prices and rates are still high enough to price some of the new buyers out of the market, but the middle of the market has become more active again. The multi-family unit is still in demand. In addition, there are still many communities that are short of apartments and other rental units. As expected, the fastest growth has been in those fast-growing cities that have been adding jobs and people such as parts of the Far West, the Northeast and southern cities like Nashville and Atlanta. There has been much slower growth in the industrial Mid-West. The expectation is that growth will slow more in 2019 as there is likely to be a period of higher mortgage rates. There are indications that new construction will start to slow due to the lack of skilled workers.

Steel Consumption

The steel markets have been volatile all year due to the confusion surrounding the tariffs. By now, we all know the basic plan and intent, but it is far from clear that any of this has been accomplished. The U.S. steel industry has been suffering for decades, and from a variety of issues—some self-inflicted such as massive pension obligations and some as a result of government decisions that chopped into their core markets. This included the demand for fuel efficient cars and the subsequent reduction in the amount of steel used in vehicles. Then there have been the delays in working on the U.S. infrastructure as this is the single biggest market for steel. In that mix was the competition from steel imports. The ostensible reason for the tariffs was to block the import of Chinese steel, but that had been accomplished years ago. China is not even in the top 10 as far as imports to the U.S. The real problem is that China accounts for over half the steel production in the world. That meant other nations that produce steel had to compete to find their own overseas markets. This usually meant the U.S. Now the top five exporters to the U.S. are Canada, Brazil, South Korea, Mexico and Russia. Right now, Brazil and South Korea have exemptions from the tariffs. It is expected that Canada and Mexico will soon get them as well. All of this has meant that prices for domestic steel have risen, but there has been little or no added capacity as the steel makers don't trust that these tariffs will remain in place.

Industrial Capacity Utilization

There has been a return to slightly higher capacity utilization this month. It is back to the peak established a month or so ago. This is still short of the supposed ideal between 80% and 85%, but it is getting closer to the 79% level. The fact that capacity has not reached into the 80s yet is probably a good thing right at the moment as this suggests that inflation is not imminent from the industrial community. When the rate of usage hits that 85% level, there will be shortages and bottlenecks. That inevitably leads to higher prices as there is increased competition for those scarce resources. The good news is there was quite a bit of added capacity in 2018, but that did not add appreciably to a utilization issue. It was assumed that it would, but that capacity was absorbed relatively quickly. This year will not likely see the kind of stimulative tax cut that 2018 saw. That will limit the amount of new capacity added.

Purchasing Managers' Index New Orders

The decline in the PMI (Purchasing Managers' Index) has been nothing short of shocking and has been causing more than a little distress. The PMI New Orders index has fallen nearly 20 points in roughly a year—from near 70 to just over 50. Another couple of points and the index will be in contraction territory (any reading below 50). The mood in the industrial and manufacturing community has soured considerably as they look ahead to 2019. The fact is most of the indicators are still trending in a positive direction, but the longer-term outlook seems far less encouraging. Each company cites slightly different reasons for their angst, but all point to issues like the U.S.-China trade war, the uncertainty surrounding the "new" NAFTA (USMCA), the impact of the government shutdown and threats of higher interest rates. The sense is that 2018 was full of stimulus and encouragement, but that 2019 will have little of that. The expectation is now tilted towards slower growth. Companies are starting to hunker down. See the chart at the bottom of this newsletter.

Metal Pricing

For much of the last year, the price of industrial metals has been falling with only the occasional reversal. Even then, the gains have been minor. This has been somewhat perplexing as there has been decent industrial growth worldwide and thus there has been demand. Then you have the price hikes that have been experienced in the U.S. due to the aluminum tariffs. The rest of the world has not seen these price hikes; instead, there may be a glut of aluminum as the U.S. users reduce their consumption in reaction to the tariffs. There has been evidence of aluminum sellers cutting their prices in order to gain some market share. There has also been evidence of these same sellers trying to expand capacity to take advantage of demand from other industrial states. The fact that metal commodities have been dropping suggests there has not been quite the robust growth that has been asserted.

Shutdown and the Joy of Flying

I was under the impression that going through airport security was about as bad as it could get. I was wrong. To be honest, there has always been a difference between the various airports and their TSA people. The most miserable experiences have always been at McCarren in Las Vegas, but I can understand why the TSA people there are so cranky. Dealing with that many drunks and miscreants would wear anybody out. The Chicago airports are typically brusque and sharp. Some of the East Coast teams seem ready to put the lot of us through a full cavity search. Then, there are the ones that seem unfailingly nice—Milwaukee, Minneapolis, St. Louis, Kansas City and Louisville stand out for me.

I flew this week—four weeks into the shutdown. I knew the Kansas City airport is not handled by the TSA but by a private contractor so they were getting paid and everything was working as smoothly as usual. Detroit was a different situation entirely. They had experienced attrition already—agents quitting to take other jobs so they would actually get paid. Those that remained were not in a good mood. I was flagged for a bag check because I had pens and pencils in my bag. There is something utterly absurd about fighting over border security at the same time that TSA agents are not being paid. If ever there was an opportunity for something nefarious, it is when you fail to pay the people providing the security. And this is not the only idiocy as the Coast Guard isn't being paid either. What really confuses me is why we are paying the legislators and the Executive when they are so clearly not doing their jobs at all.