Strategic Global Intelligence Brief for February 5, 2020

By Chris Kuehl, Ph.D., NACM Economist—

Short Items of Interest—U.S. Economy—

Trade Gap Reduced Last Year

There is good news and bad news as far as the trade deficit is concerned. For the first time in six years, the gap has narrowed. The problem is this reduction in the size of the deficit was the result of reduced imports, which occurred from the imposition of tariffs on China and other nations as well as a slowdown in the purchasing activity of consumers. We not only bought fewer imports, we bought fewer domestically produced goods. The other fly in the ointment was that exports have been down as well. The bottom line is global growth has been in decline. That hurts the U.S. (and the rest of the world). To see growth rates in the U.S. rebound, there will need to be improvement elsewhere as well.

Will Economy Be the Key in This Election?

It usually is. These are very early days and much will happen in terms of the Democratic race, but for the moment, there is a stark difference when it comes to the economy. Trump touted the state of the U.S. economy with a lot of hyperbole and bombast, but that is to be expected. The data supports the assertion the economy is doing pretty well. There are plenty of concerns for the year to come, but the start has been stronger than expected. Meanwhile, the current leader in the race for the Democrats is Bernie Sanders who advocates major economic change—free education, Medicare for all, all student debt forgiven, an end to fracking, much higher taxes on wealth and much higher taxes on fuel, much higher minimum wages and much tougher regulation.

Private Sector Keeps Adding Jobs

The official labor numbers will be released at the end of the week, but the pre-release from ADP holds that the private sector added close to 300,000 jobs. That translates into a pretty healthy gain. The vast majority of the new jobs have been added by small- and medium-sized companies. If there is a worry for down the road, it might be that larger companies are starting to engage in more layoffs and restructurings. Much of this has been due to mergers and acquisitions, but the retailers are adjusting to their new realities and are shutting down operations rapidly.

Short Items of Interest—Global Economy

China Criticized by Global Health Authorities

At first it appeared China had learned its lesson after the SARS outbreak. It was roundly criticized for the response that allowed the SARS virus to spread so rapidly. This time, it looked like China had been quick to report, but now it is evident it delayed the response for weeks and tried to downplay the seriousness. Since the outbreak, China have been reluctant to accept help from the U.S. or anyone else and it has been slow to put control measures in as it continues to downplay the threat. China is now coming under intense criticism from the World Health Organization (WHO) and other global health organizations.

Chinese Crackdown on Dissent

For a few weeks, the Chinese government seemed to tolerate the commentary by its own medical community as regards the coronavirus. There was little attempt to halt conversation, while the ordinary person was allowed to vent their frustration. That tolerance has ended as medical personnel who do not follow the party line are being censored. In many cases, they are being relieved of their duties or fired outright. Criticizing the effort is now illegal. The official party line is that everything is just fine.

Africa Worries

The most vulnerable part of the world—outside China itself—has been Africa. This is a region that struggles to deal with the disease issues it already has and lacks the capability to deal with another virus. The other issue is there is a considerable level of migration between China and Africa and to regions that are completely ill-equipped to deal with this. It is likely that the virus will end up killing more people in Africa than in China.

Does the U.S. Benefit from China's Crisis?

The comments from Commerce Secretary Wilbur Ross suggested the spread of the deadly virus in China and the rest of the world was a good thing for the U.S. as it would mean more jobs in the U.S. There is no doubt this was a morally reprehensible comment as world leaders are expected not to gloat over the deaths of hundreds of innocent people from a vicious disease, but the other question is whether it is true.

Analysis: The assumption is the coronavirus will hamper Chinese manufacturing. That will reduce their output and their exports. This could mean some other producers would be called upon to fill that gap. It is likely that most of this supply chain shift would be to other nations that compete with China (Vietnam, India, Mexico, Brazil, etc.), but there would likely be some additional output from the U.S. as well. On the other hand, the virus could well mean less business for the U.S. as has been pointed out by Trump's economic advisor Lawrence Kudlow. In the "phase one" agreement between the U.S. and China, there was an agreement from Beijing that included much more purchasing from the U.S. Now that is in question given the large number of shutdowns and the travel restrictions imposed to deal with the virus. If the Chinese experience a drastic slowdown that affects overall imports, there will be a reduction in exports from nations that buy from the U.S. That means reduced exports from the U.S. The bottom line is pretty obvious—a pandemic that kills people by the hundreds and perhaps thousands is not a good thing—for anybody.

Grand Plans in Mexico Fade

As President Andres Manuel Lopez Obrador (AMLO) came to power, he declared a grand vision for the country that would rest on the development of major infrastructure projects. They would bring prosperity to long-neglected parts of the nation, and at the same time, the country would pour money into expanded social programs to address the issues of poverty and underdevelopment. There would be a concentrated attack on the drug gangs and the Mexican economy would loosen its dependence on the U.S. economy. Now that AMLO has been in power for over a year, there has been very little progress on any of these fronts as the Mexican economy has been in a pronounced slump and there is no money for much of anything. The national rate of growth prior to the election of AMLO was close to 3%. Today, the country is in recession with negative growth numbers. The foreign investment AMLO had been counting on has vanished and the internal investors have become highly defensive and unwilling to put their money to work in the face of additional taxes.

Analysis: The infrastructure dreams were grandiose even before the economy started to shrink. Last year, the Mexican economy fell into recession with a decline of 0.1%. That didn't stop AMLO from declaring an intent to build the "Mayan Train"—a grand new route around the Yucatan peninsula that was supposed to encourage mass tourism and allow for the development of industry. This is a $7.4 billion project that was originally supposed to be half paid for by private investment. Those investors have all pulled out and now the entire cost will be borne by the government. There are other projects—a $4.2 billion airport, an $8 billion refinery, a transport corridor costing $170 million and plans to spend $530 million on 2700 additional branches of a state development bank.

The undertaking was going to be challenging from the start, but that was when there was substantial interest from outside investors. This engagement evaporated as the AMLO administration reduced and removed incentives and increased the taxes due, while simultaneously reducing the revenue opportunities. The investors moved on to other projects in other nations such as Brazil and Colombia where the returns were superior. The government in Mexico now promises to fund these efforts internally, but there is simply not enough revenue to do so. Taxes have been hiked, but these have not offset the tax loss that comes with a shrinking economy. The battles with the U.S. over trade have taken their toll as well. The U.S. push against immigration from Mexico has compromised the usual levels of remittances that made up a substantial part of the budget.

Mexico depends on four economic pillars; all are in some trouble these days. There has been a decline in remittances from Mexican nationals working in the U.S. The manufacturing sector had been the biggest moneymaker, but the trade wars with the U.S. have compromised the sector. Tourism is down due to fears over drug gang activity and the energy sector has been slowed by the lower prices for oil.

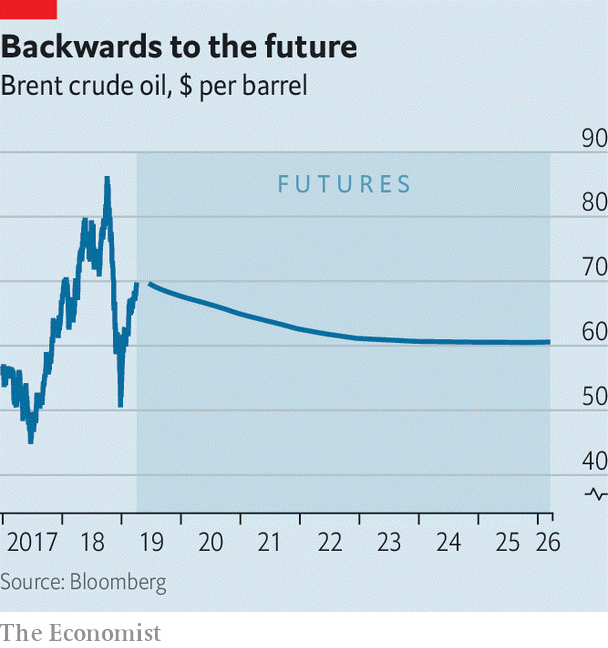

Major Changes on Horizon for the Oil Sector

The world of oil today is a far cry from anything expected even a few years ago. Remember back in the oil crisis days when the analysts were confidently predicting per barrel prices as high as $150 to $180. The price at the pump was supposed to be hitting as high as $6 or even $7 a gallon. The rise in oil prices would trigger everything from electric and natural gas-powered vehicles to an explosion in mass transit use. The U.S. consumer would reject trucks and SUVS and migrate to mopeds and SMART cars. My how things have changed.

Analysis: The oil companies are now predicting a much different future—one where the per barrel price could fall to as low as $25 a barrel. This takes the cost of oil back to levels not seen since the 1970s. The fact is new techniques for developing oil have arrived and dozens of new sources are discovered every year. Suddenly, the assumptions of just a few years ago are being rejected. The consumer is back to the large land yachts, electric cars are still a micro-market and mass transit remains an option for only a fraction of the commuting public. The pressure to add substantially to gas taxes has increased as the price at the pump has fallen. The once mighty oil nations in OPEC have lost most of their clout as the production epicenter has shifted to North and South America. It was once asserted that oil producers needed oil prices at close to $70 a barrel to remain profitable, but now it seems a profit can be sustained at prices as low as $25 to $30. There is always the possibility that some geopolitical crisis can alter the future, but given the nonreaction to the events in Saudi Arabia and Iran, it seems it will take an all-out war.

Manufacturing—In Recession or Recovery?

In the time-honored tradition of the economist, the answer to this question is yes. The manufacturing economy in the U.S. is both in recovery and in recession. It all depends on which sector of the manufacturing community one is referencing as well as what part of the country. It would seem pretty obvious there is a lot of variability in this sector. It is therefore hard to make flat statements regarding the current state of a part of the U.S. economy contributing around $2.7 billion to the annual GDP. The U.S. economy remains dominated by the service sector, but much of that service economy is in service to the manufacturers. If one counts only those workers that are actually engaged with the machines and manufacturing process, they make up around 8% of the workforce, but if you count people according to who employs them, the manufacturing share of employment jumps to over 30%. Most of the people who work for the likes of Ford, GM, Boeing or Caterpillar or the thousands of small- and mid-sized manufacturers have jobs that are classified as service jobs.

Analysis: In the broadest of terms, the manufacturing sector is in either a slow growth mode or actual recession. There had been a five-month period in which the Purchasing Managers' Index was tracking in the contraction zone (it popped back into expansion territory by a narrow margin this month). Industrial production numbers have been down in the manufacturing area, while holding steady when it comes to utilities and the mining (gas and oil) sector. Durable goods numbers have been off and so have factory orders in general. The level of capacity utilization has been under the levels considered normal for growth and capital investment has been off. Within these broader categories there has been a good deal of variability.

Again, in the broadest sense, there are seven major sectors in the U.S. manufacturing community. These are the sectors that account for the bulk of the domestic and imported output and culminate in the large assembly operations taking all these millions of parts to assemble into something for the consumer market. At the top of this list is the automotive/vehicle sector. It is followed by the aerospace sector, energy-related manufacturing, construction machinery, health care-related manufacturing, agricultural machinery and finally the appliance sector (commercial and consumer). Looking at this list, it is easy to see why there can be both progress and decline in the broader manufacturing community.

At this point in 2020, aerospace is down due to the Boeing crisis, farm machinery is down due to the travails in the agricultural sector this year and construction has suffered from the lack of investment in infrastructure. Meanwhile, health care is booming, automotive has been holding its own along with energy and the consumer has continued to drive appliance activity.

Reacting to Currency Manipulation

The new rule set by the Commerce Department will allow U.S. companies to pursue tariffs against those countries that are accused of using their undervalued currency as a form of export subsidy. This rule is not expected to make a big difference as far as trade and tariff policy as it remains very hard to prove that a currency has been deliberately undervalued by government action.

Analysis: The value of a given currency is essentially a matter of demand. If a currency is weak, it is because there is little demand for it. Demand can fluctuate for a variety of reasons, but often it is related to investment. A nation with higher interest rates will see more demand for its currency than one with low rates, so a currency's value can be affected by what the central bank does. The problem is that a lowering of rates is generally motivated by a desire to stimulate the economy and the impact on currency value is secondary. The U.S. has been lowering rates for the past decade—is that currency manipulation?

Leading by Example

Unfortunately, we can no longer look to our political leaders for much. Maybe we never could. The history books tell us that most of those who have held these positions had more than their fair share of inappropriate behaviors and hardly deserved to be held up as examples of anything but raw ambition, corruption and selfishness. That doesn't mean this is the way it should be. There have been those who deserved our admiration even as we disagreed with the decisions they made. I hail from a part of the country that lays claim to both Harry Truman and Dwight Eisenhower. I am proud of that and I am proud that they were both presidents that actually led. It seems so long ago that I could say this.

Given the rancor and overt hatred that now pervades our politics, we are going to have to find our leaders somewhere else. Maybe it will be businesspeople who work every day to do their best for employees, investors, consumers and the world at large. Maybe we will need to pay more attention to our religious leaders or to our cultural leaders. Maybe we find inspiration from some pundit or another or maybe we need to look much closer to home. Maybe we need to focus on what we can actually control—our own behavior and actions. Are we empathetic and fair? Do we have integrity and are we honest? Do we do the best we can and are we tolerant of others even when they are not like us? Being all these things and more will never be easy. We will always fall somewhat short, but the effort is still worth it.

Oil Prices

The estimates as far as oil pricing is concerned will vary a great deal according to demand and supply—that much is obvious. The factors that traditionally have the most impact include natural and manmade disasters that interrupt production, geopolitical turmoil that affects production and the overall performance of the global economy and its impact on demand.