Strategic Global Intelligence Brief for December 18, 2019

By Chris Kuehl, Ph.D., NACM Economist—

Short Items of Interest—U.S. Economy—

Industrial Activity Recovers—

The industrial production numbers include three sectors that do not always move in lockstep. The biggest part of the measurement concerns manufacturing. Of late, this sector has been slowing down. The other two categories include mining (which is mostly the oil and gas sector) as well as utilities. The latter category is generally the most stable. For the last year, the manufacturing data has been affected by all manner of issues—from the trade wars to the lengthy strike at GM. The end of that strike had a lot to do with the recovery of these numbers and the tariff war has cooled just slightly—enough to allow the manufacturing sector to adjust, Despite the good news, there is still a good deal of trepidation regarding what happens in 2020.

Fed Plans to Stay Where It Is

The statements from the Fed officials scheduled to be part of the Open Market Committee next year are sounding very unified at the moment. It is in agreement as regards the rates and do not see any reason to either lower them further or to start hiking them again. The inflation threats have not manifested in any way—no wage inflation and no commodity-driven spikes either. There is also nothing that lower rates would accomplish. The reality is rates are already uncomfortably low for small banks and too low to give the Fed any real ammunition should another downturn loom.

Tax Bill Agreed To

It ended about as expected with some agreement on extending tax breaks, reviving others and shifting some policy, but the big revamp that had been the original goal was as elusive as ever. The impact on the federal budget is significant, but far less dramatic than had been anticipated when all this began. There will be about $55 billion less coming into the coffers. That will have some impact on budget cuts, but originally, it was thought taxes would be cut by almost $500 billion. Some of the big moves involved biodiesel, railroads and medical deductions.

Short Items of Interest—Global Economy

China Continues to Throw Its Weight Around

If there was some notion that all this trade pressure would somehow bring the Chinese to heel, their actions of late should dispel that opinion. The Chinese navy has just launched its first, own aircraft carrier; several more are in development. The country has had carriers before, but they were smaller and had been purchased from other nations. This is a true-blue water vessel that will allow China to project military power anywhere in the world. At the same time, the Chinese have been cracking down brutally on the Uighur minority, while the government has been harsh towards any nation that expresses opposition to this policy. The Islamic world has not supported their Uighur brothers for fear of offending China.

Locust Swarms Devastate Crops Throughout the World

The southern tier of nations has been beset by the largest infestation of locusts seen in decades. It was a rainy spring and this encouraged breeding on a massive scale. The insects are now stripping whole regions of every bit of vegetation. They leave nothing behind as they swarm in the hundreds of trillions. In many locations, they are so thick they blot out the sun. There has been no success in stopping their advance and mass famine will follow behind.

French Confrontations Intensify

The Macron position on pension reform has been utterly rejected by the various French government unions as they aggressively guard the systems they have in place. The welter of different plans makes the French system one of the most complicated and unfair in the world. Macron wants a unified system to take its place. The current system involves some very cushy and generous provisions for specific categories—everything from bus drivers to garden maintenance workers to palace guards.

Some Generally Good Readings from the Indices

It is that time once again. We have compiled a set of index readings on behalf of two manufacturing groups—the Chemical Coaters Association International and the Industrial Heating Equipment Association. Both of these are composed of companies that work with metal for industries such as automotive, aerospace, agriculture and many more—any company that requires chemical coating or heat treating. These are some of the areas of the economy they pay close attention to. What follows is the executive summary and some of the specific assessments of the indices.

Analysis: If there is a word that describes the current business mood in the U.S., it would be hesitation. The data released of late has been a real mix; it doesn't create much enthusiasm regarding 2020. The various issues that started to worry the business community this year have yet to create huge problems, but they have become nagging concerns. The unemployment rate is very low, but that seems to have created a shortage of workers. The consumer remains in a good mood despite the trade war and the tariffs, but retailers have yet to pass on the higher costs of the goods they are importing. The manufacturing sector has been slumping for several months, but the service sector has continued to support growth. There is a little something for both the optimist and the pessimist.

Of the 12 index readings we watch, the majority are pointing in a positive direction—eight of them. The bad news is that half of these are barely moving in that direction. Of the four that are trending in a negative direction, the slump is pronounced. This is the kind of data that encourages a sense of caution and trepidation. The most positive numbers are coming from new automobile/light truck sales, new home starts, steel consumption and credit movement. Some of these gains have surprised analysts and there are questions regarding how long these patterns will remain. The auto sector has been due to slow down for two years now, but keeps defying these predictions. Its growth is a significant factor as far as steel consumption. The other sector driving steel output has been commercial construction, an area dominated by the expansion of health care. The rise of new home construction has been even more surprising given the fact Millennial buyers are still not that active. The low mortgage rates are still playing a big role, but so is the movement of Boomers into various iterations of senior living. The credit sector as measured by the Credit Managers' Index has improved in part because companies are trying to get their credit obligations under control before next year, so there has been an increase in dollar collections and a decrease in slow pays.

The other four positive indices are only barely in that category. Metal prices have been generally flat as there has been a reduction in demand for the majority of these commodities. The data from factory orders and appliance activity has also been essentially flat and this is after a period of some decline. Overall, there has been a reduction in capital expenditures. This is not unusual when there is demonstrated slack in the manufacturing sector. There is not much incentive to invest in new machinery or new facilities or hiring when the current assets are not being used to maximum efficiency. The factory orders have tapered off a little as the holiday season has gotten underway. It is obvious at this stage that retailers are not interested in doing a rush inventory recharge.

The bad news is coming in some critical index readings. The slump in capacity utilization has accelerated and worsened. That is bad sign for those that want to sell new machinery or for those seeking jobs. The numbers are not awful—still in the mid- to high-70s when ideal is 80%, but they were better even a couple of months ago. The data from the Purchasing Managers' Index has been a concern for several months now. The overall index has been in contraction territory for the last four months and the numbers are dropping. The same pattern is manifesting in the new orders index. That is the reading that points toward the future. There has been a slip in durable goods orders as well and that follows from the data on capacity as well as capital expenditure (capex). The durables market for industry has been far weaker than the consumer side, but the demand for those consumer durables will be unlikely to survive the end of the holiday period. This has been a holiday where the practical gift has been strong—a new washing machine as opposed to some jewelry. The final negative reading was in the Transportation Activity Index; it was a very slight decline. The worrying part is that transportation usually sees a strong reading this time of year. The parcel carriers such as UPS, FedEx, USPS and even Amazon and others usually see a strong end to the year. This season has been no exception. The problem is there has been decline in other sectors such as trucking, air cargo and rail. There have already been some high-profile bankruptcies in trucking and more are expected.

New Auto and Light Truck Sales

The vehicle sector has been defying predictions for the better part of a year. To some degree, the analysts have been throwing their hands in the air as they try to explain the persistence of demand. There were supposed to be all manner of headwinds affecting the sales of new vehicles, but thus far, they have not kicked in. The costs of these vehicles have been rising and financing has been getting a little harder as banks are dealing with far more bad debts than expected. The fact remains that consumers are still confident and still feel secure in their jobs. That makes them eager to buy. There are two potential issues on the horizon. The first is demand for vehicles has been very different from one age cohort to another. Nearly all the demand is still coming from Boomers and Gen-X as Millennials and especially Gen-Z are simply uninterested in owning a car. The second issue is threats of tariffs and other trade restrictions may cause a price hike that deters buyers. There have been threats to cut imported cars and parts from Japan, Europe, China, Canada, Mexico and pretty much everywhere else in the world. The auto industry asserts this could add between $5,000 and $8,000 to the price of cars—even those made domestically.

New Home Starts

The big dip in housing starts has reversed, but has not reached the previous high level. The good news is that starts are still at a higher point than they have been for the majority of the year. The growth has been primarily in the multi-family category as has been the case for the last several years, but there has also been some activity in the traditional single-family category. As with the vehicle sector, the difference in generations has been a significant factor. The Boomer is not driving sales as they once did as they shift into senior housing. There is a worry that there will soon be a glut of existing homes on the market due to this shift. The majority of home buying has been from Gen-X, but the older Millennial is staring to get interested in the single-family option as they decide to have kids. The least interested generation thus far has been the Gen-Z as they are still too young and seem uninterested in leaving their parent's homes. The regional differences are also profound—more housing interest in the South and Midwest.

Steel Consumption

The sharp rise in steel consumption has taken analysts by surprise although it has been noted this gain only brings the consumption numbers back to where they had been. The three areas that stimulate steel consumption are vehicle manufacturing, construction and, to a lesser extent, durable goods and appliances. All three of these sectors have shown some signs of growth in the last month with commercial construction leading the way. There has not been a big surge in public sector activity thus far, but there are many major projects underway throughout the U.S. These commercial gains have been primarily in health care, hospitality and entertainment as office projects are still limited compared to the demand exhibited in past years. There are persistent rumors that big infrastructure projects will be funded by Congress in the new year, but these have not materialized as yet. Agricultural machinery remains in a slump as well.

Industrial Capacity Utilization

This is not a good trend and it seems to be accelerating. The measurement is critical as it suggests when companies are likely to start investing and expanding. As long as they have slack capacity, they are not likely to buy new machinery, add more people or look at expansion into new territories. Once they get to the point of full capacity, they will be encountering bottlenecks and shortages. That is a trigger to start looking at these additional purchases and more hiring. The "ideal" percentage is between 80% and 85%; lately the index has been sinking. The numbers do not yet scream crisis, but the decline has accelerated and is certainly heading in the wrong direction. This adds to the sense that many manufacturers are preparing to enter the coming year with some trepidation and caution.

PMI New Orders

The data from the Purchasing Managers' Index (PMI) has not been encouraging for the last few months. The overall index has been in the contraction zone for four months in a row. Granted, the numbers have not been deep into the 40s, but it was less than a year ago that the index was hitting high 50s and even 60s. The sense is that caution and fear have taken root in the manufacturing sector as there are continued concerns regarding issues such as trade wars, tariffs and the uncertainty of an election year. The business community is deeply worried that the choices in the U.S. election will be miserable—a continuation of the mercurial and anti-trade policies of Trump or the high taxes and expanded regulation promised by the left-leaning Democrats. This trepidation is starting to show up in the more future-oriented index from the ISM. The new orders numbers have also been in contraction territory for the last four months.

Capital Expenditure

The pace of capital expenditure has leveled off over the last several months—this comes as a shock to nobody. The reduction in capacity utilization would have suggested this was a possibility. The three areas of capex have all been affected. There has been less in the way of investment in machinery, less investment in facility expansion and reduced levels of inventory. The inventory-build through much of last year disguised the reduction in spending in the other areas. The manufacturers had been reacting to the trade war with China and the anticipated shortages of needed material so there was a build-up in inventory. Now that process has been largely completed, affecting some of these capex numbers.

Durable Goods Shipments

The durable goods numbers are down as well—no surprise here. When there is a decline in both capital investment numbers as well as the capacity utilization data, it stands to reason the production of goods designed to last three years or more would also see some downward movement. These are generally goods that are for business purposes, but also includes the longer-lasting consumer goods such as appliances. The business community has been exhibiting a very cautious attitude as they look ahead to 2020. There is nothing that really signals a significant decline and certainly not an impending recession, but there is concern about issues such as the slowing global economy, the impact of all the trade wars and the lack of certainty regarding the elections in the U.S. There is simply too much uncertainty for companies to make long-term decisions.

What Does It Mean to Age?

To begin with, it certainly beats the alternative, but it does go beyond this. As I get older, I notice my friends and relatives are doing the same and that sometimes shocks me. This is especially the case with people I have not seen in a while. They should look and act like they did the last time I saw them, but that is never the case. I think about my age now—more than I used to and I notice age more than I used to. At the same time, I do not feel old (although my body will disagree on that point). I am well past retirement age, but this is the furthest thing from my mind as my business partner and I plan the next 10 or 20 years for Armada. I have always focused on the future and have rarely thought about the past; that remains my habit. My wife is nearly 12 years older than I am and is just as future oriented with the full expectation that we have decades to come. Maybe we don't, but we will live as if we do.

It has been said over and over that age is just a number, but it is also an attitude. I have friends of my age and younger who are quite definitely "old." They have all but stopped their lives and just seem to be waiting out the rest of their days. This saddens me as I am convinced they have much to look forward to. I know there are things I can't do as I used to and there are some things I no longer want to do, but there are far more adventures to anticipate and goals I yet want to pursue. But right at this very moment, I mostly want to turn in early and wait for my cats to wake me up at 5:00am tomorrow.

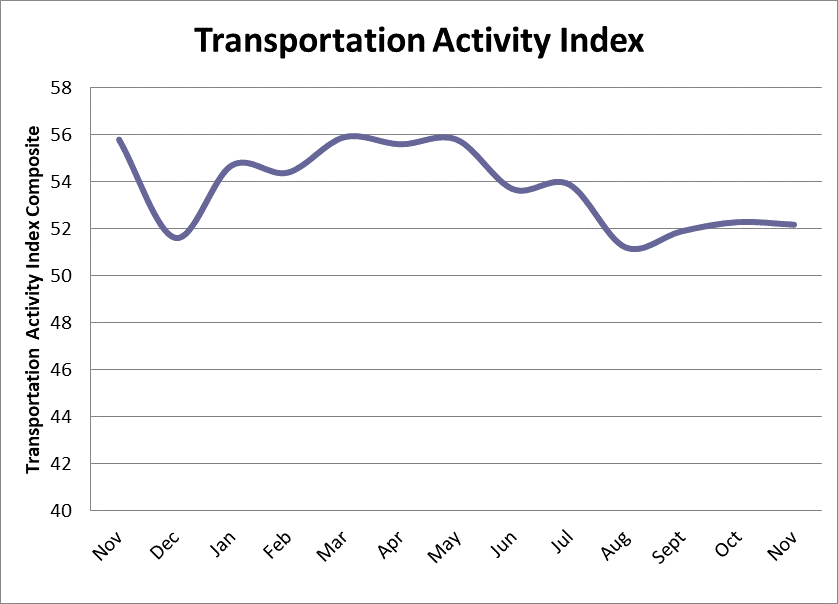

Transportation Activity Index

The canary seems to have recovered a little. The transportation sector has long been viewed as something of an early warning system. Movements in a positive direction for the economy tend to show up in additional demand for trucks, trains and planes. Likewise, when there is a general economic slowdown, the need for transportation services dwindles. The sector had been in decline for several months, but there now seems to be a reversal underway and a small pickup in activity. This month saw a very slight retreat from the month prior, but both months have been better than September. One note to be aware of is the disproportionate influence of the parcel carriers this time of year. The heavy delivery schedule for UPS, FedEx, USPS, Amazon and the like will tend to skew the data for transportation this time of year.