Strategic Global Intelligence Brief for April 8, 2019

Short Items of Interest—U.S. Economy

Budget Fight Looms

In October, the two-year deal struck by Congress expires. That means Congress will need to develop a new budget by that point or watch the process revert to what it was two years ago. This would bring back the sequester, which would mandate a cut in the budget of 10% for the 2019 period. That will amount to a $125 billion reduction. At this stage, it is nearly impossible to see the current Congress reaching any kind of accord as positions are about as distant from one another as they have ever been. The one thing that could force through some kind of deal is the looming pressure of the election in 2020. If Congress fails to get something passed and these cuts go ahead, there will be some very angry constituents. That would play into the campaigns very quickly.

The Week for Inflation Data

Before the week is out, the U.S. will have some more data with which to assess the inflation threat. The Consumer Price Index (CPI) comes out on Wednesday and the Producer Price Index (PPI) on Thursday. The expectation is that not a great deal has changed, but there will be attention paid to some of the sub-sector data. The CPI rose a little last month due to energy prices and food prices. This is a trend that may continue this month. The PPI is also expected to react to changes in the price of energy as well as some of the other industrial inputs. There have also been some modest gains in the last few months. The expectation is for another 0.3% increase.

Wage Growth Slows

It was certainly good news that the jobs data bounced back last week and there was creation of another 196,000 jobs, but there were some cautionary notes in that data as well. The recovery from the really weak numbers in March suggests that companies are doing all they can to hire people and expand. The fact that wage growth slowed at the same time, however, suggests that these new hires are not as qualified as would be preferred. The hope had been that wages would increase as that is the expected pattern when the jobless rate is this low. New hires are not commanding much higher wags because they are not ready to contribute right away. They have to be trained. During that training they will not be making that much money.

Short Items of Interest—Global Economy

Signs of a Libyan Takeover

For most of the last few years, it has been seen as only a matter of time before General Khalifa Haftar made his move. He has controlled the eastern half of the country for the better part of two years and has been systemically wiping out all opposition. Now he has started to attack the capital in Tripoli and has leaked plans for his assault in the rest of the country. The U.S. and most European states are pulling their people out. The expectation is that the country will be enmeshed in a civil war. The impact on oil prices has been limited, however, as the nation has been ripped apart for years.

Radicalized Britain

The future of Brexit is not all that is at stake. The Brexit crisis has meant the end of Theresa May as prime minister. She has hung on this long as nobody wants the job right now, but she will go down as soon as the deal (whatever it is) is complete. The two most likely leaders are then going to be Boris Johnson (leader of the pro-Brexit Tories) or Jeremy Corbyn (Labor Party). They are both radicals in terms of traditional British foreign policy. Johnson is the U.K.'s Trump and will ally with the populists in the U.S. and in the rest of Europe. Corbyn is the unabashed socialist who has been termed the U.K.'s Bernie Sanders. He will likely ally with the remains of the harder left in the EU and the world in general.

Netanyahu Unpopular but Winning

The Israeli polls suggest that Prime Minister Benyamin Netanyahu is deeply unpopular, but even those who dislike him plan to vote for him as they fear the alternative.

Forming an Anti-Immigration Coalition in Europe

Regardless of the lack of logic, it has become a political fact that immigration has been used by the right-leaning populists to galvanize support throughout Europe and the U.S. The immigrant flood into Europe has been blamed for virtually every ill that besets the region, but few take the time to determine if this set of accusations even makes sense. The fact is immigration has captured the attention of the electorate in a way no other issue has. In country after country, the immigration debate has created new and very popular political parties that have scarcely mentioned any of the traditional issues that once defined politics in Europe in favor of focusing on the threat posed by immigration.

Analysis: It is a real problem that has been blown significantly out of proportion. Since the collapse of the regimes of various Middle Eastern and North African strongmen (Saddam Hussein in Iraq, Muammar al-Gaddafi in Libya, Bashar al-Assad in Syria and so on) there have been vast populations in search of some modicum of safety and security. This is a wholly new kind of immigration for the European to contend with. In the past, the people making their way into Europe were essentially just seeking jobs. They were overwhelmingly males and their intent was simple enough. Only a small percentage planned to remain in Europe for long. They wanted to make a lot of money and then return home. On average, they planned to stay for between one and five years. As the region started to disintegrate politically, the motivation for migration changed. Now it was whole families, women with small children, the elderly and so on. They were no longer economic migrants—these were refugees fleeing war and violence. They have no idea when they will be able to return home and they have little opportunity to work or fit in with the new society. They immediately become dependent and have to receive aid from the nations where they are now. This breeds resentment among those in the host nations that have been demanding help of their own as well as from those who are being taxed to pay for that help.

There are many other motivations for the resentment that has been building for years. There are those who despise the newcomers because of their cultural differences, their race and ethnicity. There are fears that there are terrorists among those who have fled to Europe and further fears of more "ordinary" violence. Given the level of frustration within these refugee communities, it is not unusual for there to be outbreaks of violence among people who have had their lives utterly destroyed. All of these hostilities and resentments have fueled the rise of populist movements throughout Europe—Alternative for Deutschland, Sweden Democrats, National Front in France, Danish People's Party, Finns Party and the Northern League in Italy. The latter party is part of the ruling coalition in Italy—paired up with the Five Star Movement. The power of the populists has been growing with every passing year. Most assume that more governments will include populist parties in a ruling coalition. The populists were behind the U.K.'s decision to withdraw from the EU. These same populist ideas fuel the Trump base.

While the focus is on immigration, there has been very little attention paid to the issues of economic development and growth. Europe's economy has been sclerotic at best. The jobless data shows a decline in hiring and most of the business sentiment indices are weaker than was the case only a year ago. This has been a major factor in the decline of growth—even apart from the impact of Brexit and what this has done to trade.

Europe Frustrated With China as Well

The world has been focused on the ongoing trade war that threatens to engulf the U.S. and China, but the reality is that many other nations have been struggling with the way China comports itself. For the past five years, the Europeans have been trying to put together a deal with China, but nothing has come of it thus far. The major issue is the same one that has vexed the U.S.—Chinese subsidies and support for those industries that compete in the global market. The EU is not prepared to go after China with tariffs as the U.S. has—it has determined that this ultimately hurts their own companies as much or more than it does the Chinese. It has started to lose patience and will be seeking ways to make the Chinese less comfortable with the choices they have been making.

Analysis: In many ways, the Europeans will be waiting to see what happens as far as U.S.-China deals are concerned. If the U.S. is able to wring concessions out of China, the Europeans will attempt to piggy-back and demand the same arrangements be made for them. It allows the EU to stand back and let the U.S. do the dirty work.

Dodging the Bullet

It has been said more than once that economists have managed to predict 16 of the last three recessions. It is true that when given a choice between a gloomy prediction and one that is all sunny and optimistic, the majority of economic analysts will fall into the glass half-empty category, and for the most practical of reasons. If one assumes there are people who pay attention to the musings and analysis of the economist, it is because the information is meant to be predictive. It is supposed to help a company or individual or government make intelligent decisions regarding what might be coming. The intent is obviously to be as accurate and predictive as possible, but this is the study of human behavior after all—there are lots of variables. Inevitably, there will be some missed predictions. They will fall into one of two categories. Either the prediction was overly optimistic or it was overly pessimistic. In the great scheme of things, it is better to be pessimistic and wrong than to be optimistic and inaccurate. Nobody will really get upset over conditions being better than they were expected to be.

Analysis: If one looks at the data that was coming out through the last several months of 2018 and early 2019, it was understandable that analysts would start to get concerned. Although last year had started strong and was propelled along by the early tax cut, the impact of that series of breaks had been fading. By the end of year, it had mostly fizzled as a motivator. The performance of the retail sector in the fourth quarter was not what had been expected given the growth seen earlier in the holiday season. There was a slowdown in 2019 as job growth and the various trade and tariff issues had been taking their toll on some of the more vulnerable sectors. Global growth was also affected by a sharp slowdown in China as well as in Europe. The Chinese estimated growth to have fallen to just over 6%, which is recession in an economy like China's. The eurozone growth rate had fallen to under 1% and Germany was at 0.7%. It appeared that the bulk of the developed world would be facing at least a significant slowdown and perhaps even an actual recession. The assessments coming from the economic analysts were gloomy, but most acknowledged there was still time to reverse the pattern or at least ease the sting of this advancing slowdown.

It is certainly not the case that all of these concerns have evaporated in 2019, but there have been some definite improvements as far as the global economy is concerned. There has not been the deterioration that had been expected in the U.S. by this time. The abrupt collapse in terms of hiring in February convinced many that the U.S. economy has indeed run out of steam and there would be further decline in the rate of hiring. This fear was dismissed (at least temporarily) by the data that has emerged since with job growth numbers close to 200,000. Not everything is rosy as far as employment is concerned as too many of these jobs are in low-paid sectors of the service industry, but there is still hiring taking place. That is generally a good sign. The biggest worry about jobs is that needed skills are in very short supply. It has been common for business to hire people who are less than qualified for the jobs they have been hired to do. This is something that will show up in productivity data sooner than later.

The U.S. is not expecting robust growth from the first quarter, however. The consensus view is that growth numbers will be down to as low as 1.3%. Thus far, the second quarter is not coming in as much more positive. Much of that growth will depend on what happens in other parts of the world. Here, the news has improved slightly. The Chinese started to see a little recovery in their manufacturing sector. That will boost the nations that traditionally sell to the Chinese. The export sector for the Chinese seems to have stabilized a little as the U.S. has held off on the next round of tariffs—at least for the time being. Meanwhile, there has been an aggressive attempt to open up new markets in other parts of Asia as well as emerging market economies in Latin America. These will not be able to replace the U.S. market for Chinese goods, but it has softened some of the trade war blow. Europe has also seemed to avert the worst. It looks as if the EU nations have been able to adjust to the changes under Brexit. This is now seen as a problem for the British, but not one that matters as much to Europe as these nations still have one another and have diversified their markets better than the U.K. has. Does all this mean the threat of recession has been avoided? To some degree, that seems to have been the case, but there are still plenty of issues that will slow economic progress.

And Now for Another Perspective

Not everybody believes that the threat of recession has been dodged. At best, many think that the development of deeper problems has been delayed and perhaps only for a short time. The International Monetary Fund is referring to all this as a synchronized slowdown and predicts that a global slowdown has gotten underway already. This is a development that will require a similarly focused effort to avoid. The sense is that developed nations will have to institute some kind of mass stimulus that is coordinated between them so that every region of the world is affected.

Analysis: There are many issues that will serve to block an effort like this. The most obvious is there is a lack of stimulative capacity in the developed world. The central banks have not been able to hike their rates. That leaves them no room to lower them now. The various legislatures have budget issues and simply do not have the spare cash that would be needed to spend their way out of a recession. It means they have to borrow. Most of these nations are already running very significant debts and deficits. Beyond all that, there is the question of how this additional money would be spent. How would these extra funds be used to fend off a recession? More public works, more money in people's pockets, more welfare?

Treated as One Would Like to Be Treated

I live in a neighborhood that more or less exists in two worlds. It is a part of the city that once had the reputation of decline and poverty, and parts of it still do. On occasion, I get a very clear picture of how attitude and behavior can be shaped by perception. I bank with a large institution with branches all over town. They are most definitely not all alike. The one nearest me is part of that older neighborhood and the staff is generally more suspicious and hostile. Despite having been with this bank for over 40 years, I encounter times when my paychecks are held for up to a week. I no longer go to that branch as another branch in a more affluent neighborhood never questions my check deposit. The people at the local grocery store are markedly less friendly and more suspicious than those at a grocery store on the other end of the county. I get annoyed at being treated this way and begin to understand the frustration of people who get this lack of respect every minute of every day.

I do understand that these businesses may encounter more problems than in other areas, but it seems a self-fulfilling prophecy. You treat people as potential criminals and you will not convince them to show much concern or loyalty. It would seem that one could give people the benefit of the doubt, but that approach seems rare indeed.

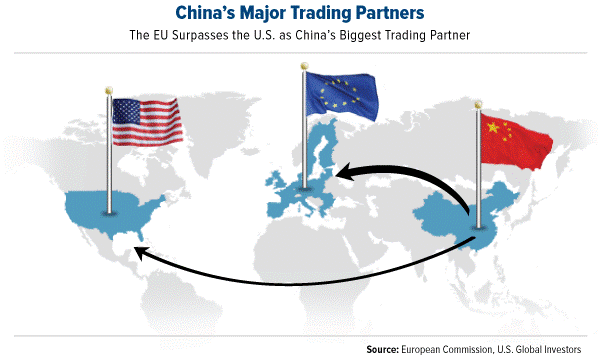

China's Major Trading Partners

The Chinese are actually more dependent on trade with the EU than they are with the U.S. It is a bigger export and import relationship. In the wake of the new antagonism between the Chinese and the U.S., it is expected that EU-China will become an even bigger deal. That has meant there is a lot at stake when EU-China trade talks resume.