Week in Review

Global Roundup

February 10, 2020

Week in Review

Global Roundup

February 10, 2020

How coronavirus is affecting the global economy. The coronavirus outbreak is already having a damaging economic and business impact, affecting everything from tourism to the supply of parts to the automotive and technology industries. (HSN)

China to cut tariffs on $75 billion of U.S. goods. China said it would slash tariffs on $75 billion of U.S. imports in half as part of its effort to implement a recently signed trade agreement with Washington. (HSN)

Zimbabwe to liquidate exporters’ forex. The Reserve Bank of Zimbabwe (RBZ) says it will liquidate all foreign currency that will be channeled into the country after the prescribed three-month period for exporters in a desperate attempt to shore up foreign exchange flows in the country. (The Standard)

Coronavirus could hurt German economy due to its reliance on China. Since the coronavirus outbreak started, the Chinese economy has begun to suffer. As a result, Germany, and particularly its car industry, could also lose out as China is its most important trading partner. (EurActiv)

Just how stable is Hong Kong’s economy? The financial centre faces protests, a trade war and now the coronavirus. (Economist)

U.K. seeks big tariff reductions in U.S. trade deal. Britain is seeking far-reaching reductions in tariffs from a trade deal with the United States, Trade Minister Liz Truss said on Feb. 6, setting out the broad aims of a post-Brexit push to secure new free-trade agreements. (HSN)

Russia foreign minister visits Venezuela as U.S. warns of sanctions reprisal. Venezuelan President Nicolas Maduro holds talks with Russia’s foreign minister on Feb. 7 as Moscow continues to support the isolated South American nation’s socialist government despite Washington’s warnings that it may ramp up sanctions. (Reuters)

IMO 2020 fuels the sustainable transition of the shipping sector. The deadline for the much-anticipated IMO 2020 regulation has arrived and with it comes a new set of challenges, potential solutions and newfound awareness of the impact this will have on all players within the shipping sector—from shippers to fuel suppliers. (Global Trade Magazine)

Modern Monetary Theory: Cash-strapped governments a thing of the past? States with a currency of their own can never run out of money. That's a core thesis of the Modern Monetary Theory which spilled over to Europe from the U.S. (DW)

Protectionism mars progress on Africa-wide free trade area. Growing protectionism and nationalism are identified as the greatest risk to the African Union’s prospective continent-wide free trade area, with negotiators facing an uphill struggle to meet July’s target for becoming operational. (Global Trade Review)

The costs of Colombia’s closed economy. Importers must run an obstacle course for products imported by Colombia. (The Economist)

Europe braces for negotiation storm in 2020. The EU’s negotiating skills and unity will be put to a series of tests this year as the bloc seeks to thrash out a deal with the U.K. and minimize the impact of Brexit, conclude a trade agreement with the U.S. and finalize its long-term budget for 2021-2027. (EurActiv)

Incoterms 2020 CPT: Spotlight on Carriage Paid To. Incoterms 2020 rules outline whether the seller or the buyer is responsible for, and must assume the cost of, specific standard tasks that are part of the international transport of goods. In addition, they identify when the risk or liability of the goods transfer from the seller to the buyer. In this article, Shipping Solutions discusses the Incoterm CPT, also known as Carriage Paid To. (Shipping Solutions)

Grand Plans in Mexico Fade

Chris Kuehl, Ph.D., NACM Economist

As President Andres Manuel Lopez Obrador (AMLO) came to power, he declared a grand vision for the country that would rest on the development of major infrastructure projects. They would bring prosperity to long-neglected parts of the nation, and at the same time, the country would pour money into expanded social programs to address the issues of poverty and underdevelopment. There would be a concentrated attack on the drug gangs and the Mexican economy would loosen its dependence on the U.S. economy. Now that AMLO has been in power for over a year, there has been very little progress on any of these fronts as the Mexican economy has been in a pronounced slump and there is no money for much of anything. The national rate of growth prior to the election of AMLO was close to 3%. Today, the country is in recession with negative growth numbers. The foreign investment AMLO had been counting on has vanished and the internal investors have become highly defensive and unwilling to put their money to work in the face of additional taxes.

The infrastructure dreams were grandiose even before the economy started to shrink. Last year, the Mexican economy fell into recession with a decline of 0.1%. That didn't stop AMLO from declaring an intent to build the "Mayan Train"—a grand new route around the Yucatan peninsula that was supposed to encourage mass tourism and allow for the development of industry. This is a $7.4 billion project that was originally supposed to be half paid for by private investment. Those investors have all pulled out and now the entire cost will be borne by the government. There are other projects—a $4.2 billion airport, an $8 billion refinery, a transport corridor costing $170 million and plans to spend $530 million on 2700 additional branches of a state development bank.

The undertaking was going to be challenging from the start, but that was when there was substantial interest from outside investors. This engagement evaporated as the AMLO administration reduced and removed incentives and increased the taxes due, while simultaneously reducing the revenue opportunities. The investors moved on to other projects in other nations such as Brazil and Colombia where the returns were superior. The government in Mexico now promises to fund these efforts internally, but there is simply not enough revenue to do so. Taxes have been hiked, but these have not offset the tax loss that comes with a shrinking economy. The battles with the U.S. over trade have taken their toll as well. The U.S. push against immigration from Mexico has compromised the usual levels of remittances that made up a substantial part of the budget.

Mexico depends on four economic pillars; all are in some trouble these days. There has been a decline in remittances from Mexican nationals working in the U.S. The manufacturing sector had been the biggest moneymaker, but the trade wars with the U.S. have compromised the sector. Tourism is down due to fears over drug gang activity and the energy sector has been slowed by the lower prices for oil.

-

APRIL

24

11am ET -

Where the Buck Stops: Establishing KYC &

Export Compliance Best Practices

Speaker: Paul J. DiVecchio, principal of DiVecchio & Associates

Duration: 60 minutes

-

Just a Little off the Top: Strategies for Reducing the Growing Cost of B2B Credit Card Acceptance

Speakers: Lowenstein Sandler Partner Andrew Behlmann and

Colleen Restel, Esq.

Duration: 60 minute -

APRIL

29

3pm ET

-

MAY

7

11am ET -

Collections 101

Speaker: JoAnn Malz, CCE, ICCE, Director of Credit, Collections, and

Billing with The Imagine Group

Duration: 60 minutes

-

Author Chat: How to Lead When You’re Not in Charge

Author: Clay Scroggins

Duration: 90 minutes | Complimentary -

MAY

8

11am ET

Businesses Face Political and Environmental Risks in 2020

With 2019 being marked by a rise in protectionist rhetoric and the first decline of global trade in 10 years, trade credit insurer, Coface, anticipates that international trade will grow by only 0.8% in 2020.

The truce trade agreement between the United States and China is unlikely to restore corporate confidence or significantly boost industry and world trade, especially as only 23% of the protectionist measures taken between 2017 and 2019 affect the United States or China, Coface says. The rise in protectionism is therefore a global and lasting trend to which companies will need to adapt.

The trade credit insurer does not expect global growth to recover this year. It shrank to 2.4% after 2.5% in 2019. Coface expects corporate insolvencies to increase in 80% of the countries for which forecasts are issued this year, including United States (3% in 2020), the United Kingdom (3% in 2020, after a cumulative increase of 17% since the June 2016 referendum), Germany (2%) and France (1%). Overall, Coface anticipates a 2% increase in insolvencies worldwide, in line with 2019.

Uncertainties related to the protectionist environment also contribute to the volatility of commodity prices, particularly those of agriculture, metals and oil. According to Coface's forecasting models, steel prices will continue to fall over the next six months, penalizing companies in the sector, especially as growth in China—which accounts for half of global steel demand—is expected to reach only 5.8% this year. Therefore, the metals sector risk assessment has been downgraded in five countries, including the United States and Italy. Moreover, the sustained low level of oil prices, despite geopolitical uncertainties (USD 60 per barrel of Brent on average in 2020 after USD 64 in 2019) will hurt some indebted producers, notably in the United States.

On the bright side, the construction sector is benefiting from highly expansionist monetary policies: Its assessment has been upgraded in four countries (including Brazil and Turkey). In total, Coface downgraded 22 and upgraded eight sector assessments this quarter, reflecting the significant increase in risks for the economy.

The end of 2019 saw an increase in social tension “trouble spots” around the world, with varying levels of intensity. This underlying trend was strongly anticipated by the Coface Political Risk Index, published at the beginning of 2019 and is at an all-time high. In 2020, this indicator forecasts a high level of social risk in several countries in Africa, the Middle East, Central Asia and even Russia.

Since 2019, social discontent has also manifested in increasing demands for environmental protection. Environmental risks have a wide range of effects on corporate credit: greater frequency of physical risks (natural disasters arising from climate change), but also transition risks (new and more stringent regulations, changes in consumer standards). For the latter, the effects of stricter anti-pollution regulations for the automotive sector in India or in global shipping must be monitored this year. Coface pays close attention to the analysis of these two categories of environmental risk.

Growth in emerging economies should accelerate slightly this year (3.9% versus 3.5% in 2019). However, public debt has reached a historically high level for these countries and is increasing in all regions except Central and Eastern Europe. In Latin America, the level of indebtedness is higher than at the end of the 1990s, which was a period marked by recurrent debt crises. In Africa, public debt is close to the level observed around 15 years ago: a period of debt write-offs by international and bilateral donors. For companies in these regions, this means that government and large State-Owned Enterprises (SOEs) arrears are likely to increase this year. The only good news is that the structure of emerging countries’ sovereign debt is generally more favorable than 20 years ago, since 80% of it is now denominated in local currency.

In this delicate and volatile environment where economies are facing headwinds, four country assessments have been downgraded (Colombia, Chile, Burkina Faso and Guinea), while six have been upgraded (Turkey, Senegal, Madagascar, Nepal, Maldives and Paraguay).

Outlook for Latin America and the Caribbean:

New Challenges to Growth

Alejandro Werner

Economic activity in Latin America and the Caribbean stagnated in 2019, continuing with the weak growth momentum of the previous five years and adding more urgency and new challenges to reignite growth. Indeed, real GDP per capita in the region has declined by 0.6% per year on average during 2014–2019—a sharp contrast from the commodity boom’s average increase of 2% per year during 2000–2013.

Regional challenges

Elevated policy uncertainty in several large Latin American countries continues to weigh on growth. For example, uncertainty about the course of economic policy and reforms in Brazil and Mexico likely contributed to the slowdown in real GDP and investment growth in 2019.

Continued economic rebalancing in stressed economies that experienced sudden stops in capital flows in 2018-19 (Argentina, Ecuador), while helping restore internal and external balances, have also acted as a drag on economic growth.

More recently, a few countries in the region experienced social unrest—Bolivia, Colombia, Chile and Ecuador—which, in some cases, disrupted economic activity. Economic policy uncertainty has also risen in these countries as governments consider alternative policies and reforms to make growth more inclusive and address social demands.

Outlook and risks

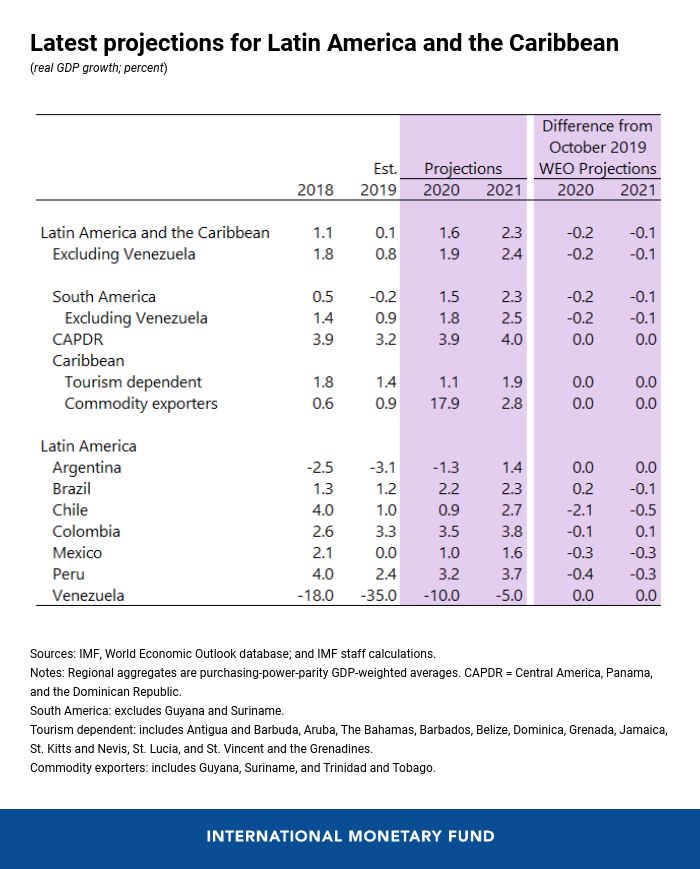

As noted in the recent World Economic Outlook update, growth in the region is projected to rebound to 1.6% in 2020 and 2.3% in 2021—supported by a gradual pickup in global growth and commodity prices, continued monetary support, reduced economic policy uncertainty and a gradual recovery in stressed economies.

However, there are also prominent downside risks. While previous external downside risks have moderated following globally synchronized monetary policy easing and the signing of the U.S.-China phase one trade deal, some new risks have appeared, including the potential global spread of the coronavirus, which could significantly disrupt global economic activity, trade and travel. Domestic and regional downside risks have also intensified. Social unrest could spike throughout the region, while economic policy uncertainty could rise further due to both heightened social tensions and policy slippages.

Policy priorities

Economic policies will need to strike a balance between rebuilding policy space and maintaining economic stability on the one hand and supporting economic activity and strengthening the social safety net on the other hand.

Although the causes and triggers of social unrest have varied across countries, they generally reflect discontent with some aspects of the economic and political systems. A key priority going forward is to reignite growth, while making it more inclusive. Promoting competition will be important to avoid monopolistic practices that may hurt the poor disproportionally. Tackling corruption and weak governance will help make political systems more representative, although deeper political reforms may be needed.

Fiscal policy will need to support growth, expand the social safety net and improve the quality of public goods and services. However, in many countries, spending room in the budget remains constrained by high deficits and public debt. These countries will need to improve spending efficiency, reallocate spending from nonpriority areas to public investment and social transfers and increase revenues over the medium term to finance additional increases in these areas.

Monetary policy can remain accommodative to support growth given the stable inflation outlook, well-anchored inflation expectations and declining neutral rates worldwide.

South America:

In Brazil, growth remained subdued at 1.2% in 2019, but is projected to accelerate to 2.2% in 2020 due to improving confidence following the approval of the pension reform and lower monetary policy interest rates in the context of low inflation. Steady implementation of the government’s broad fiscal and structural reform agenda will be essential to safeguard public debt sustainability and boost potential growth.

In Chile, the outlook is subject to uncertainty resulting from social unrest and the evolving policy responses to the social demands. Following a sharp decline in late 2019, economic activity is expected to recover gradually supported by a significant fiscal expansion and looser monetary policy, with growth reaching about 1% in 2020.

In Colombia, strong domestic demand led to a pickup in growth to 3.3% in 2019 and a widening of the current account deficit to 4.5% of GDP. Growth is projected to accelerate to around 3.5% in 2020 due to continued monetary support, migration from Venezuela, remittances, civil works and higher investment due to recent tax policy changes.

In Peru, growth is estimated to have slowed to 2.4% in 2019, hampered by lower global trade and under-execution of government spending. With these factors dissipating in the coming years, growth is projected to recover to 3.2% in 2020 and 3.7% in 2021, with inflation remaining well-anchored within the central bank’s target range.

Venezuela remains immersed in a deep economic and humanitarian crisis. Since the end of 2013, real GDP has contracted by 65% driven by declining oil production, hyperinflation, collapsing public services and plummeting purchasing power. A continuation of these trends is projected for 2020, although at a slower pace. The acute humanitarian crisis has led to one of the largest migratory crises in history, with migration to neighboring countries expected to surpass six million—20% of the population—by 2020.

Mexico, Central America, and the Caribbean

In Mexico, economic activity stagnated in 2019 due to policy uncertainty and slower global and U.S. manufacturing production. Growth is expected to recover to 1% in 2020 as conditions normalize, including with the ratification of the trade agreement between the United States, Mexico and Canada (USMCA) and the recent easing of monetary policy, which should continue as along as inflation expectations are well-anchored. Fiscal policy should be geared at putting the public debt-to-GDP ratio on a downward trajectory, with priority on increasing revenues, improving the efficiency of spending, and enhancing the fiscal framework.

In Central America, Panama and the Dominican Republic growth is projected to rebound to 3.9% in 2020, from 3.2% in 2019, supported by the beginning of operations of a large copper mine in Panama, and accommodative monetary policy in Costa Rica and the Dominican Republic. In Costa Rica, continued implementation of all measures in the fiscal reform bill will be key to rebuild market confidence and fiscal space.

In Honduras, the economic plan includes important efforts to improve institutional, governance and anti-corruption frameworks supporting business confidence, while Guatemala is expected to continue benefitting from a fiscal impulse and economic reform plans of the new administration. El Salvador is already reaping the effects of the pro-growth agenda of the new administration inaugurated in June, while unfavorable political tensions in Nicaragua are creating a significant headwind to economic recovery.

In the Caribbean, economic prospects are improving, but with substantial variation across countries. Growth in tourism-dependent economies is expected to strengthen in 2020. With commodity prices remaining broadly stable, commodity exporters are expected to see modest recovery in growth, while large oil discoveries and the start of their production in 2020 is expected to boost growth in Guyana.

The region’s exposure to climate risks continues to require strong policies. Potential growth continues to be impeded by lingering structural problems including high public debt, weaker financial systems, high unemployment and vulnerability to commodity and climate-related shocks. Some countries have started to strengthen their fiscal positions, but further tightening is needed in others to ensure debt sustainability.

Reprinted with permission from IMFBlog.

Reprinted with permission from IMFBlog.

Week in Review Editorial Team:

Diana Mota, Associate Editor and David Anderson, Member Relations